- Oil Scenario

Another commodity to suffer a rollercoaster ride is crude oil, levered up by Trump’s armada sailing towards Iran, and pushed down by the perceived risks of engaging these forces. It would invite unquantifiable retribution from the Ayatollah’s missile forces and the damage they could do to Israel and to US bases across the region.

The fragility of the situation was highlighted this week in the Arabian Sea when a US F-35C warplane shot down an unmanned aircraft that was allegedly “aggressively approaching” the USS Abraham Lincoln.

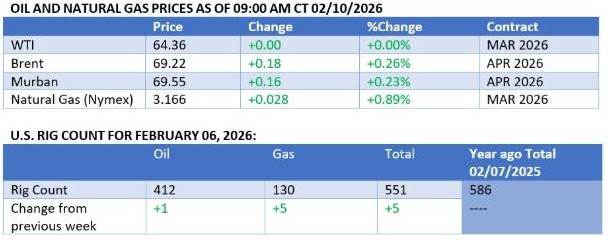

Oil prices spiked higher, reflecting the risk of possible closure of the Straits of Hormuz that would lead to a major oil shock.

Despite this, diplomatic talks between the US and Iran continue with Iran requesting that they be moved from Turkey to Oman and be limited to discussing its nuclear program and the lifting of sanctions, resisting pressure to include its ballistic missile program and its support of regional armed militias. This request looks like a stalling tactic causing Trump to warn Khamenei on Thursday that “he should be very worried”.

Large crude oil tankers appear to be taking all this noise and volatility in their stride. US and EU enforcement against dark fleet tankers hauling sanctioned Russian, Iranian and (until recently) Venezuelan crude oil has tightened the market measurably. Uncertainty has been created by US tanker seizures in the Atlantic, Iranian tanker arrests in the MEG, and Ukrainian attacks against Russian tankers and oil facilities in

the Black Sea. Hence, the risks of loading sanctioned oil and ships have risen.

The newly struck US-India trade deal carries with it the expectation that India will cease, or more likely cut back, its purchases of Russian oil. India likes to tread a delicate path between Washington and Moscow, hoping to get on with both, so it is unlikely to completely abandon Russian product, and its refiners are now said to favour diversity of supply, not only discounted prices. Traders expect Russian oil flows to India to taper down to 0.8-1.0m-bpd, half of what they were at their peak.

Bloomberg, reports that millions of barrels of unsold

Iranian and Russian crude are accumulating in storage as buyers shift to legit barrels.

With Brent trading in the $60-71 a barrel range this year, the calculus may be that buying the illicit stuff is not worth the bother. Safer to buy slightly dearer unsanctioned oil and use compliant tankers. Such cargoes can be sourced from the MEG, USG and Latam on VLCC’s and Suezmax tankers, including 0.8m-bpd of now unsanctioned Venezuelan exports.

Estimates, the black-market Russian & Iranian glut at 100-plus million barrels, split between onshore and floating storage, worth at least $5bn, with 58mb of the total stored afloat.

Beyond more effective US and EU sanctions and political pressure, buyers of sanctioned crude oil have plenty of alternative sources at currently acceptable prices, and playing by the rules carries a smaller cost.

Buyers of sanctioned oil, notably India and Turkey, have been switching with ease over the last 60 days to unsanctioned

barrels. This has made the mainstream oil market tighter, putting a floor under prices.

China and India are the key buyers of sanctioned oil and with Brent at $68 today it is 13% more expensive than it was in early January.

India will at least pretend to toe the US line, whereas China will not. China already purchases circa 95% of Iranian crude exports and 60% of Russia’s. The black market would not exist without China.

It is a symbiotic relationship: Iran and Russia sell their product, supporting their war economies, while China secures bargain prices as well as significant political leverage in the Middle East and Moscow.

In January, China increased its purchases of Russian crude to near record levels, partly to offset its loss of Venezuelan oil. It can buy whatever barrels India and Turkey do not take by utilising its large and expanding strategic petroleum reserve.

Beijing’s next move will have profound implications for the global market. If it declines to mop up the black-market glut, then Russia and Iran will have to cut output, pushing up global prices. Buying more of the illicit crude would enable it to cut its purchases of non-sanctioned barrels, raising availability and potentially forcing prices down.

In conclusion: “Not for the first time, Beijing finds itself in a position of influence over strategic resources.”

Meanwhile, tanker owners, particularly of large COT’s, are smiling all the way to the bank.

Nice while it lasts.

- Indian Economy: Goldman upgrades India 2026 growth forecast to 6.9%, from an earlier projection of 6.7%, buoyed by lower tariffs on exports under the framework of an interim trade agreement with the U.S. Earlier, Moody’s Ratings projected India’s GDP to grow 6.4% in FY27, the fastest pace among G20 economies, driven by strong domestic consumption.

- India may keep Chabahar presence even as sanctions loom. India is working on a playbook to Operate the Chabahar port in Iran after the US waiver on sanctions against Tehran ends in March, two people aware of India’s stance to balance ties with its longtime Persian Gulf trade partner and the world’s largest economy.

· Tata Steel hunts for iron ore as legacy mines’ leases to end

Firm meets 100% of iron ore needs from six legacy mines, but leases start expiring from 2030.

For years, iron ore was one thing Tata Steel never lost sleep over. Owning captive mines meant predictable supply, stable costs and a structural edge over rivals who depended on

expensive mines acquired through auctions or remained at the mercy of the markets.

This is, however, set to change, as the company will lose the edge when its legacy mining leases begin to expire starting 2030. To secure a stable supply for iron ore, the key raw mater- ial to make steel, the company has cast a wide net that stretches from the cold mountains of Labrador in Canada to the Gadchiroli forests in Maharashtra.

“Maharashtra, Canada, all these are options to post 2030,”, CEO of Tata Steel told on Monday, describing the company’s efforts at securing iron ore supplies. This, he said, was in addi- tion to the mines it has acquired in India under the new auction regime.

Tata Steel, the oldest steelmaker in Asia, currently meets 100% of its iron ore requirements in India through its six legacy mines awarded to it before the Mines and Minerals (Development and Regulation) Amendment Act, 2015, which requires all mines to be auctioned, rather than nominated by the government.

India’s second largest steelmaker has joined hands with a key player in central India’s mineral ecosystem, who has managed to successfully mine iron ore—and will soon also be making steel from this ore—in a Maoist conflict-prone region that few businesses dared to venture into.

In December, Tata Steel acquired a 50.01% stake in Thriv- eni Pellets Pvt Ltd. (TPPL), forming a joint venture with Lloyd Metals & Energy Ltd. TPPL, owns 100% stake in Brahmani River Pellet Ltd. (BRPL) that operates a 4 million tonnes per annum (mtpa) pellet plant at Jaipur, Odisha, along with a 212-km slurry pipeline. Pellets are small, hardened balls made of iron ore and used in steel production.

More importantly, the steelmaker also signed a memorandum of understanding with Lloyds Metals & Energy to explore min- ing opportunities in Maharashtra to increase the production of iron ore. “We are seeing opportunities as the Maharashtra gov- ernment looks at the entire Gadchiroli area for development and for mining, we will be keen to participate and understand,” said Koushik Chatterjee, CFO, Tata Steel. It is also evaluating how it can partner with Lloyds on the steelmaking side, he said.

The steelmaker has also tapped into its Canadian subsidiary, Tata Steel Minerals Canada. In January, the company flagged off a test shipment of iron ore from Canada for its domestic operations. While the shipment is yet to reach Indian shores, it could be one of the solutions to the firm’s iron ore quandary beyond 2030.

The costs that Canadian iron ore adds in terms of logistics is offset by its superior quality. The ore from Labrador has iron content of above 67% and less than 1% of alumina impur- ity. Low alumina iron ore is considered superior in steelmaking as it improves blast furnace productivity.

The firm plans to blend higher grade ore with domestic raw material to improve the charge it puts in blast furnaces. “So, it’s an option we have, which we want to test out well before 2030, so that we can decide on our plans for Canadian mine depend- ing on its utility for India”.

· ‘IOC, HPCL buy Venezuelan oil through trader’

State owned IOC and HPCL have jointly bought 2 million barrels of Venezuelan crude oil — the second deal Indian refiners have struck since oil restarted flowing into international markets.

The two firms have bought 2 million barrels of Merey crude from Trafigura for delivery in the second half of April, sources said. 1.5 million barrels of oil will be delivered to IOC’s Paradip refinery in Odisha and rest 5,00,000 barrels to HPCL’s Visakhapatnam unit in Andhra Pradesh. This is the second deal for Venezuelan crude after Reliance Industries bought 2 million barrels of Venezuelan oil for April delivery from Vitol.

The world’s third largest oil consumer halted Venezuelan crude purchases after U.S. sanctions were reimposed. It resumed imports after the U.S. granted Vitol and Trafigura a licence to sell Venezuelan oil after President Nicolás Maduro was seized in a military operation and Washington asserted control over the nation’s energy industry.

India imported Venezuelan crude until 2019/20 before U.S. sanctions on the South American country’s state oil company PDVSA stopped that. It resumed purchases in 2023/24 but hal- ted them again when Washington reimposed restrictions on Venezuela’s oil sector.

*Iran hardens crackdown on political dissidents after US talks* It extended Nobel peace laureate’s prison sentence + detained several prominent reformist figures. The crackdown’s escalation came despite US-Iran talks, which sounded positive note | 2nd round of talks planned this week.

*US tells American ships to keep away from Iran amid tensions* US-flagged vessels should stay as far as possible from Iranian waters while navigating the Straits of Hormuz after a ship was harassed last week: US advisory issued Feb 9.

*Fear of higher oil prices may push Trump to settle with Iran: RBC,* citing discussions with regional observers. Trump backed off on Greenland demands when faced with sharp market selloff, Yet Israel’s Washington visit, lingering

differences with Tehran, could tilt scales to favour military engagement.

*US boards Venezuela-linked oil tanker in Indian Ocean* after cat-and-mouse chase, Aquila II departed Jose terminal in early Dec and appeared bound for China. Ship intercepted while heading toward Sunda Strait between Indonesian islands Java and Sumatra.

*Carlyle’s Currie says oil markets are “substantially underinvested”* and have significant upside. Jeff Currie added that the glut narrative weighing on crude prices is overblown Up to 100Mb could re-enter market if sanctions were imminently rolled back, a difficult to execute scenario “nobody expects,” he said.

Sanae Takaichi’s election victory in Japan may bolster her assertive stance vis-a-vis China, but the Japanese Prime Minister must weigh her mandate against Beijing’s red lines over Taiwan. The dispute poses a dilemma for Chinese leader Xi Jinping on how to engage with Japan, a key US ally in Asia.

In Thailand, the unexpected victory for the pro-royalist Bhumjaithai Party is set to bring stability after years of political upheaval. Anutin Charnvirakul rode a wave of nationalism fuelled by simmering tensions with neighbouring Cambodia and is likely to choose caution over transformation in

addressing Thailand’s economic challenges.

· Box trade defies geopolitical turmoil with strong 2025 growth

Global box volumes rose 4.7% in 2025, outperforming muted forecasts despite geopolitical and trade policy headwinds.

Asia drove growth, led by Southeast Asia, while transpacific volumes weakened under US-China tariff pressure.

Emerging markets strengthened their role in global trade, with Sub-Saharan Africa, South and Central America, and the Indian Subcontinent posting some of the fastest growing import and export volumes.

Predictions of a sluggish year for container shipping proved wide of the mark in 2025, as global volumes rebounded strongly despite escalating geopolitical and economic pressures.

· No shortage of targets for French

interdiction | Container shipping prepares for old ships shake out | Shipping shares outperform broader stock market

At least 25 shadow fleet tankers* flying false flags transited the western Mediterranean between November and January.

Container lines are preparing for another overcapacity phase as a big wave of newbuilding deliveries coincides with moderating demand growth and a gradual return to the Red Sea and Suez Canal.

Every shipping segment is outperforming the S&P 500 index, with most segments doing much better.

· Maersk expands orderbook with China ULC newbuilds

Maersk confirms firm order for eight 18,600 teu ultra-large containerships at New Times Shipbuilding, with deliveries scheduled for 2029-2030.

The LNG dual-fuel vessels were first rumoured last November

and form part of Maersk’s long-term fleet renewal strategy. Chinese shipbuilder Hengli Heavy Industries has confirmed new contracts for four large crude tankers, comprising two VLCCs and two suezmax vessels.

· Confidence in LNG carriers rises as US-

Greek plans to supply Europe move forward

US hails Greece as trusted ally key to energy plans.

New Greek LNG importer says country will require a second FSRU. Tsakos says time to stop demonising LNG as marine fuel.

Shipping is critical to new ‘vertical corridor’ through Greece to

provide LNG to Ukraine.

LNG shipping involves the specialized maritime transport of liquefied natural gas, cooled to -162°C to reduce its volume by 600 times for efficient bulk transport. As of early 2026, the market is navigating short-term spot rate weakness while preparing for significant long-term growth driven by rising U.S. exports and European energy security demands.

Key Aspects of LNG Shipping:

Vessels: Modern LNG carriers, often dual-fuel, carry liquefied gas in specialized tanks at extremely low temperatures, with capacities often exceeding that of aircraft carriers.

Market Trends (2026): While spot rates hit lows in early 2025, the market is experiencing a “reset” driven by increased demand for US LNG in Europe, with 2026 projected for significant expansion.

Technology & Safety: Advanced insulation, re-liquefaction plants, and boil-off gas management are standard. Many new ships are dual-fuel, supporting decarbonization efforts by allowing the use of cargo as fuel.

Key Players: Major industry participants include Nakilat, which boasts one of the world’s largest LNG fleets, as well as firms like Eni and Eastern Pacific Shipping.

The industry is rapidly evolving due to geopolitical shifts, moving away from long-term contracts toward more complex, demand-driven shipping routes.

· Eni celebrates Congo LNG Phase 2 first cargo

The President of the Republic of Congo, Denis Sassou N’Guesso, and Eni’s CEO, Claudio Descalzi, have attended the ceremony marking the first cargo of LNG from the Nguya FLNG floating facility, signalling the start-up of gas exports from Phase 2 of the Congo LNG project. This represents a further step toward Eni’s target of expanding its LNG portfolio to 20 million typ by 2030, leveraging the flexibility, competitiveness and geographical diversification of its equity projects, and is a key milestone in building a leading position in the global LNG market.

With Phase 2, the Congo LNG project reaches a total liquefaction capacity of 3 million tpy of LNG, equivalent to 4.5 billion m3/y of gas, leveraging gas resources from the Nené and Litchendjili fields in the offshore Marine XII license.

Descalzi commented: “We reach a very important milestone thanks to the relationship of trust built with the country’s institutions and local communities. We have been the only company to invest in gas to develop the domestic market and to reduce routine flaring. This decision, taken more than 20 years ago, led us to discover enough volumes to enable export as well. Phase II of the Congo LNG project was delivered in

record time compared with industry averages, increasing gas availability on international markets and contributing to Italian and European energy security, while at the same time generating concrete benefits for the local economy.”

Congo LNG highlights Eni’s ability to transform gas resources into strategic value for the country and for international markets, through a cost-competitive project with strong environmental performance. Phase 1 of Congo LNG, launched with the Tango FLNG liquefaction unit, reached start-up in December 2023, just over one year after the project definition. Phase 2 start-up, in turn, comes only 35 months after construction of the Nguya FLNG unit began, setting a new international industry benchmark in terms of execution speed and efficiency.

· New Zealand moving closer to LNG import terminal

The government will contract to build an LNG import facility in a critical step to strengthen New Zealand’s energy security and support economic growth, Energy Minister Simon Watts says.

The decision follows extensive analysis and the first stage of procurement.

“New Zealand is experiencing a renewable electricity boom, but a rapidly declining gas supply has left our electricity sector exposed during dry years, when our hydro lakes run low,” Watts said.

“The result is greater reliance on coal and diesel, and ultimately higher electricity prices, putting more financial pressure on families and making businesses less competitive.”

Independent analysis from Sense Partners found that higher energy prices have had a significant impact on the New Zealand economy, leading to a NZ$5.2 billion loss in GDP in 2025.

“For Kiwis, that means fewer jobs, lower wages, and a slower recovery as New Zealand emerges from a challenging period of high inflation and high interest rates,” Watts added.

“In the last two years, the government has taken a series of positive steps designed to improve the affordability and availability of energy, as part of our plan to fix the basics and build the future.

“That includes fostering greater competition through tougher regulation of major energy companies and enabling greater development of New Zealand’s natural resources to unleash the supply of renewable and non-renewable energy.

“Establishing an LNG import facility is an important next step.”

The LNG import facility will provide a reliable backup fuel source, reducing the impact of dry-year risk on electricity pricing and stabilising electricity costs. It will also add another layer of resilience by giving New Zealand access to additional supply options if domestic gas supply tightens unexpectedly.

“Just having a reliable back up is expected to save Kiwis around NZ$265 million/y by reducing price spikes and lowering the risk premium built into power bills that exist because of supply challenges, equivalent to around NZ$50/y per household,” continued Watts.

“If domestic gas supply continues to decline and drive-up gas prices, the availability of LNG is estimated to be worth NZ$1.2 billion/y to the New Zealand economy by 2035. Access to LNG is also expected to protect around 2000 jobs from the economic impact of rising energy prices and gas shortages.”

The government has shortlisted leading proposals and is progressing to commercial contracting, with the aim of signing a contract by mid-2026. The facility could be operational as soon as 2027 or early 2028.

“Located in the Taranaki, the project will create jobs during

construction and provide long-term skilled roles once

operational, reinforcing the region’s role at the heart of New Zealand’s energy system,” Watts concluded.

Access to LNG will support many gas-dependent industries to consider their long-term energy needs and invest accordingly, by reducing the risk of supply disruptions and extreme price volatility.

The government will design an import model that brings LNG in large shipments and only when needed, minimising exposure to international gas prices and keeping the door open for new technologies.

EU-Owned Tankers Ship 35% of Russia’s Oil in January Ahead of the EU Ban

The strategic shift of EU’s LNG imports demand is re-drawing the global LNG shipping map. Europe’s decision to formally sever its remaining gas ties with Russia marks the end of a chaper that has defined the Continent’s energy system for decades. Framed by sanctions, the move reflects a deeper structural shift. One the phase ban on Russian pipeline gas and LNG is fully implemented by late 2027, the supply gap left by Russian volumes will be covered predominantly by seaborne flows.

· QatarEnergy mapping out ‘Phase 3’ of huge LNG carrier shipbuilding project

But parallel analysis in play regarding the disposal of older tonnage

Middle East producer QatarEnergy is expected to move forward with a third tranche of LNG carrier newbuildings under its massive shipbuilding project as the company grows out its access to modern tonnage.

Multiple industry players at the large LNG 2026 exhibition and conference in Qatar last week recounted that they had been informed that plans are being developed for Phase 3 of the project.

· Sinokor becomes the world’s ‘super operator’ of supertankers

Sinokor’s stunning raid in the tanker markets over the past two months is making the Korean shipowner the largest operator of VLCCs in the world.

Sinokor’s recent purchase of potentially over 50 secondhand VLCCs, plus the company’s securing of a significant volume of tonnage under time charter, has been the talk of the tanker markets all year.

Analysis by broker BRS suggests by the time all its ships are delivered, Sinokor will control 118 VLCCs either through ownership or under time charter. This represents 13% of today’s active VLCC fleet and when excluding the 179 units assessed as being part of the grey fleet, this implies that Sinokor controls 16% of the mainstream VLCC fleet.

“There has never before been a single VLCC operator with such a dominant market share of the active fleet,” BRS stated in a recent report, updating its chart of the world’s top VLCC operators (see below).

Today, the top ten VLCC owners in the world control a combined 392 units, giving them a 42% global market share in the supertanker sector, according to BRS data. When excluding the 179 tankers BRS deems as grey, the top 10 VLCC owners combined control 53% of the active mainstream fleet and a significant 59% of mainstream tonnage younger than 20 years old.

“Although this evidence suggests a degree of consolidation, perhaps the most significant implication of Sinokor’s spree is the emergence of it as a super operator with the tonnage under their control dwarfing that of their competitors,” BRS noted.

Rival Fearnleys described the Korean company last week as

the “Kingpin” of the VLCC trades.

Splash has reported repeatedly this year on how Sinokor, in tandem with Mediterranean Shipping Co (MSC), has been on an historic VLCC acquisition binge, paying over the odds for a record-breaking amount of tonnage.

New York-listed VLCC major DHT discussed Sinokor’s market- altering moves in its latest quarterly earnings last week without referring to the Korean owner by name.

“A fundamental shift in fleet ownership is taking place with fleet consolidation by private actors gaining meaningful traction. We expect the aggregators to soon control at least 25% of the compliant tramping VLCC fleet – a critical market share. This consolidation will likely shift the pricing dynamics and put pressure on timely availability of ships,” DHT noted.

· Nordic American cashes in on oldest suezmax at hefty premium

Nordic American Tankers has sold its oldest vessel, the 2003- built suezmax Nordic Pollux, for $25m, underlining the strength of the secondhand tanker market for vintage tonnage.

The Japan-built 150,103 dwt tanker was sold debt-free, with the full proceeds going straight to the New York-listed owner.

Shipping analysts at Swedish investment bank SEB said the achieved price was well above expectations. Based on recent broker assessments and straight-line depreciation, SEB had valued the vessel at around $18m, implying the sale came in roughly $7m, or about 40%, above its estimate. The price is also around 2.5 times the ship’s scrap value, which SEB puts at about $9.5m.

“Although the confirmed price is significantly higher than our valuation, we note that transactions for suezmax tankers at this age are rare,” SEB said, adding that the deal has limited read- across to its tanker net asset value estimates due to Nordic American’s relatively young fleet profile.

The sale follows a string of disposals as the Herbjørn Hansson- led company continues to renew its fleet. Late last year, Nordic American booked a solid gain after selling two older suezmaxes, built in 2004 and 2005, for a combined net price of

$50m.

At the same time, the owner has been stepping into new steel. Earlier this year, Nordic American firmed up contracts for two suezmax newbuildings in South Korea, converting previously announced preliminary agreements into firm orders. DH Shipbuilding has been named as the builder, with the two crude tankers priced at $86m apiece and scheduled for delivery in 2028.

· Danaos steps into bulker newbuilds with newcastlemax order

Greece’s Danaos has stepped into bulker newbuildings for the first time, unveiling the move as part of a six-ship order programme that widens both its fleet mix and investment reach.

The New York-listed owner disclosed the deals alongside stronger-than-expected earnings, confirming orders for two newcastlemax bulkers of about 211,000 dwt each, with delivery slated for 2028. The contracts mark Danaos’ first direct shipyard orders in the bulker segment.

Led by John Coustas, Danaos has already built a foothold in dry bulk through secondhand acquisitions and now controls a fleet of 11 capesize bulkers.

At the same time, the owner has firmed up construction of four mid-size container vessels in China, extending a recent run of boxship investments. Danaos confirmed it has ordered four 5,300 teu containerships at CSSC’s Huangpu Wenchong Shipyard, with deliveries scheduled for 2028 and 2029.

Danaos currently counts 75 boxships with a combined capacity of 477,491 teu. With the latest orders included, the company’s orderbook now stands at 27 vessels.

On a fully delivered basis, Danaos said its fleet would comprise 102 containerships with an aggregate capacity of about 652,041 teu, alongside 13 dry bulk vessels, with a total capacity of roughly 2.37m dwt.

The fleet expansion comes as Danaos continues to further diversify beyond liner shipping. In January, the company disclosed a strategic investment in the Alaska LNG project, marking its first move into the energy sector and underlining a

broader push to spread earnings across multiple shipping and energy segments.

· Industry’s doom-and-gloom PR is sinking seafaring

Carl Martin Faannessen from crewing agent Noatun Maritime calls for an urgent need to start changing the narrative about careers at sea.

Our industry is painting itself into a self-made corner. Why? Because we are not adept at marketing, in every sense of the word.

What other industry would:

- Take every opportunity to talk up concerns

around “mental health” and “wellbeing” in a profoundly negative light? Not to mention leaving the definition of these to whoever wants to talk about it?

- Highlight “harassment and bullying” as a key topic at every event, with no mention of the flip-side of officers at all levels now terrified of cracking a joke or giving clear feedback to the people they are responsible for developing? (Whistleblower channels are now being used to apply pressure on the very people responsible for the safety, growth and development of the crew.)

- Tag along with all the providers of “woe awaits us” – programs, leaving the rest of the world with the impression that seafaring is a one-way path to a life of struggle and hazard, both physically and mentally?

To spell it out: in our eagerness to come across as well- meaning, caring, and utterly in tune with the zeitgeist we are making the career of seafaring unattractive. We talk about attracting and retaining generation this, generation that, millennials. The fact that we even buy into the concept of generation-this-that-or-the-other is telling: that someone born a

year after someone else should be profoundly different is right up there with astrology.

We combine this with pleas for help to make seafaring attractive as a profession. It takes a special kind of mental contortion to land where we are. And yet, we are now in a corner we are busily painting ever smaller.

Where are the voices arguing the counter-narrative here?

- The fact that seafaring is a much safer and more lucrative career than almost anything available in the home countries of the majority of the world’s seafarers?

- The fact that you can work 40 years, earn good money, raise a family, all in an industry governed by international conventions? With insurance coverages most of your compatriots at home ashore can only dream of?

- The fact that the vast majority of the world’s shipowners

and managers genuinely care for their seafarers?

We need to flip the script. We need to focus on the meaningful rewards and profound opportunities offered at sea. We need to highlight the countless stories of personal growth, the journeys to financial stability, the calm of the endless horizon, the team spirit built onboard, the immense scope for learning, the room to shift from ship to shore and back, and so much more.

Can we get on with this, please? Maybe make it a weekly column, where someone from the industry spends a page explaining how amazing it all is? As Bjørn Højgaard, CEO of Anglo-Eastern, once said: “I started off chipping rust.”

· Fake Vanuatu registry exposes wider epidemic of fraudulent flags

| 20 |

Vanuatu has warned of a fraudulent website impersonating its registry.

The unauthorised website, operating under the

domain registervu.com, copied content from Vanuatu’s own

registry site.

Vanuatu is not alone among Pacific island nations being targeted for false flag operations. The Tonga government, for instance, issued a statement last month denouncing any foreign vessel claiming to fly its flag. It said Tonga’s international registry of ships was closed in 2002 and the kingdom does not register foreign vessels engaged in international voyages.

Last year, Splash reported on the creation of the Maritime Administration of Matthew Island, a flag created on a 0.7 sq km rocky outcrop (pictured) where there are no inhabitants.

Matthew Island is located in the South Pacific, 300 km east of New Caledonia and southeast of Vanuatu. The island is claimed by Vanuatu, and considered by the people of Aneityum as part of their custom ownership, but also claimed by France as part of New Caledonia.

Nearly 300 tankers are flying false flags according to data from Israeli maritime analysts firm Windward.

The company has identified 18 such fraudulent registries, noting that 91% of vessels using these fraudulent registries were already sanctioned by Western authorities.

The most frequently used fraudulent registries were Guinea (51 ships), Netherlands Antilles (45), Guyana (44), and Aruba (24).

“False flags weaken the commercial and legal infrastructure that global shipping depends on to function predictably,” Windward stated in a recent update.

Recently the West has started to crack down on shadow vessels – the US apprehending 10 tankers linked to

Venezuelan trades over the last seven weeks, while France boarded a Russian Aframax last month flying a false flag in the western Mediterranean.

· Trading giant Vitol tied to twin Greek product carrier deal

Major Shipowner and Charterer appears to be parting ways with several vessels.

Just a few weeks after being tied to the sale of up to three

modern LR2 tankers, trading giant Vitol may be about to offload a pair of older, smaller product tankers as well. According to several broker reports, Greek interests are spending between

$48.5m and $49m combined on the 51,400-dwt Elandra Fjord and Elandra Baltic (both built 2011).

· Bourbon pockets $38m as two platform supply vessels are sold via online auctions

Difference in bidding activity for offshore player’s AHTSs and PSVs highlights where buying interest lies in offshore sector Two of French offshore operator Bourbon’s unwanted platform supply vessels have been sold for $19m each on the Zhejiang Shipping Exchange’s Shipbid platform.

The 4,100-dwt Bourbon Clear (built 2012) and 4,300-dwt Bourbon Front (built 2011) each attracted a single bid on their first auction attempt, falling short of the excitement seen in other recent Bourbon sales where multiple bidders drove prices far above the opening price.

· Trafigura speeds up bulker shipments from major African port

Trader agrees on first delivery of copper and cobalt to global markets via Lobito Atlantic Railway. Trader Trafigura is stepping up bulker exports from the Angolan port of Lobito.

The Charterer and Shipowner said it had agreed the first

delivery of copper and cobalt to global markets in a deal with Democratic Republic of Congo (DRC) state group Entreprise Generale du Cobalt (EGC).

The shipments will leave the terminal after arriving via the Lobito Atlantic Railway (LAR).

· Kamsarmax bulker up for grabs in online auction on Chinese platform

Auction on the Guangzhou Shipping Exchange on 12 March will open at slightly below its market value

A Kamsarmax bulk carrier will be offered for online auction with a minimum price of $22.78m, under its market value.

The 82,000-dwt bulk carrier CCS Orchid (built 2017) is being marketed by the Guangzhou Shipping Exchange for sale via online auction.

Online registration for bidders closes at 14.00 Beijing time (06.00 GMT) on 12 March, with the timed bidding window running from 16.00 to 16.30 Beijing time (08.00 to 08.30 GMT).

· Hapag-Lloyd profit hit by falling rates and new network costs

Preliminary results at higher end of forecast as launch of Gemini alliance depresses full-year result

Hapag-Lloyd’s profit has slumped because of lower freight

rates, higher network costs and rerouting of vessels.

Operating profit (Ebit) fell to $200m in the fourth quarter of 2025, compared with $800m a year earlier, according to preliminary results released today.

Ebitda slumped to $800m from $1.4bn, while revenues dipped

$400m to $5bn.

- The electronic bill of lading: are we at the tipping point?

THE electronic bill of lading has been one of the most talked- about innovations in container shipping for years now.

Advocates say it can slash costs, cut fraud and ultimately unlock an entirely new world of digital trade finance. Sceptics

say we’ve been hearing that promise for a decade and paper still dominates.

The latest DCSA figures put global EBL adoption at around 11%. That’s growing, but it’s a long way from the 100% target that carriers have set themselves for 2030.

So where do we actually stand? To find out, APAC editor Cichen Shen sat down with two people at the centre of the shift: George Guo, the chief executive of IQAX, one of the two largest eBL providers in the world by volume; and Peter

Hartz, Maersk’s head of ocean surcharges, value-added services and energy products.

· Oil Runs Deep

Aberdeen, with its windswept views of the North Sea, has for decades carried the title of Europe’s oil capital. After vast offshore reserves were discovered in the 1970s, the Scottish city transformed from a modest fishing port into a booming economy with one of the UK’s highest concentration of millionaires.

For Paul de Leeuw, an engineer who first came to Aberdeen more than three decades ago, tapping the North Sea’s wells rivalled the complexity of putting a person on the moon. “I wanted to be part of that journey,” he said, recalling his work for companies including BP and Shell. “Aberdeen was a thriving hub.”

Yet that status has been slipping for years, sharpening a political fight in Westminster over whether the industry is even worth salvaging at this point. As the green transition accelerates, oil and gas production in the UK, much of it tied to Scotland, has fallen to less than a quarter of its peak in Britain’s slice of the aging North Sea basin. Aberdeen’s job market is now among

the weakest in the UK.

To many opposition leaders, the prescription is straightforward: lift exploration bans and roll back taxes they argue have damaged the sector. Last year, no company began drilling a new exploratory well in the UK, the first such pause since the 1960s, according to Wood Mackenzie.

Rio Tinto and Glencore have abandoned plans for a $260bn megadeal that would have created the world’s largest mining group.

Baltic Shipping News 10th February, 2026

Baltic Dry Index: 1882 (-13)

Baltic Capesize Index: 2771 (-62)

Baltic Panamax Index: 1670 (22)

Baltic Supramax Index: 1123 (9)

Baltic Handysize Index: 646 (7)

BCI 182 TC AVG $/DAY 25128 (-564)

BPI82 TC AVG $/DAY 15027 (+198)

BSI TC AVG $/DAY 14200 (+123)

BHSI TC AVG $/DAY 11623 (+130)

CAPESIZE

The Capesize market saw a relatively busy Tuesday, yet it still closed in negative territory. The C5TC 182 eased by $564, finishing the day at $25,128. In the West Africa/Brazil region, activity picked up as more fresh cargoes emerged for first half March loading. Two fixtures were concluded at $22.75 last night, though gossips today indicated lower levels being fixed which led the C3 route to close at $22.35. The Pacific opened with two majors in the market but sentiment remained soft.

Market talk pointed $8 and gradually sub $8 levels from operators.

Atlantic

The Mount Lhotse (211,919 2025) eta Tubarao 10/11 March was rumoured to have fixed at $22.10 basis C3. An unnamed vessel was linked to ENBW’s 160,000/10 Drummond to Ijmuiden and Amsterdam 1/10 March at $15.35.

Asia

There was talk of CSE taking a Newcastlemax for 165,000/10 Port Walcott to Taiwan 1/5 March at $8.00. Mercuria was linked to taking a Newcastlemax for 190,000/10 West Australia to Qingdao 24/28 February at $7.85. Ningbo Marine reportedly fixed a TBN for 130,000/10 Newcastle to Liuheng 1/10 March at a rate in the low/mid $12s. Vale fixed a vessel for 170,000/10 TRMT to Qingdao 22/24 February in the high $5s.

PANAMAX

As we move into the week, sentiment across both the Atlantic and Pacific has turned more constructive, with freight levels on key routes showing early signs of improvement. Atlantic activity is firming, supported by an increase in prompt trans-Atlantic enquiries as charterers seek near-by tonnage, lending support to rates. Grain fronthaul supply from EC South America remains steady, while cargo availability from NC South America appears healthier, with additional support from an active US Gulf market. In contrast, mineral cargo interest remains limited despite some talk of some US East Coast to India business. In Asia, activity has picked up on the longer duration voyages, while Indonesian business appears relatively subdued. The P5TC average increased by $198 to settle at

$15,027.

Atlantic

Olam fixed on a TBN for a 75,000/10 coal stem from Baltimore to Paradip 1/10 March dates at $34.00 fio from

Messrs Avani.

Asia

An Oldendorff TBN was reported to have fixed a 75,000/10 coal stem loading from Dalrymple Bay into Dhamra 1/10 March at $13.25 fio with Trafigura. The Emmy (82,151 2023) fixed delivery Taizhou 12/14 February for a NoPac grains round voyage at $15,250 with Norden, whilst the Yangze 15 (82,027 2019) fixed from Ube for an Australian run into India at

$14,500. The Princess Grace (75,455 2020) was reported to have been placed on subjects basis Zhoushan following drydock 15/16 February for an Australian grains into the Arabian Gulf, and the scrubber fitted Bright Venture (81,487 2020) was also on subjects basis delivery Hong Kong 15/17 February for a trip via Indonesia to Japan. The Safeen Al Safa (81,874 2012) Songxia 19/21 February and RG Athena (82,282 2007) Hong Kong 9 February were both reported also to be on subjects but further details lacking.

Further cover included the Fjeld Svea (81,583 2013) fixing ex Lianyungang 17/18 February for delivery North China to Japan trip at $14,000s with Oldendorff. The Axios (81,960 2017) open Onahama 13/16 February was linked to a NoPac round voyage with petcoke at $15,000 although the charterer remained undisclosed. The SFL Pearl (81,659 2012) Xiamen 14 February was heard fixed for a trip from Australia into India and the Kiyo (92,353 2012) fixed basis Shanghai 13 February for an Indonesia round with Messrs Fullinks. Cargill was also reported to have covered a NoPac grains stem from 1 March onwards but no more details emerged.

SUPRAMAX

Positive gains seen again from the US Gulf, brokers saying tonnage availability remained tight for February putting increasing upward pressure on rates. The South Atlantic on the other hand remained rather lethargic and brokers said it remained finely balanced. Elsewhere, an Ultramax was heard

fixed basis delivery Egypt Mediterranean to the US East Coast at around $11,000 but no more details came to light. Also, a Supramax was rumoured fixed basis delivery Canakkale via Ukraine for a trip Singapore-Japan at $12,000 again no more details came to light. More of the same from the Asian arena, as a lack of demand from Indonesia and limited fresh enquiry further north saw rates ease once again. The 11TC did however remain in positive territory increasing $123 to $14,200.

HANDYSIZE

The market displayed another day of mixed performance, with some regions holding steady while others saw stronger gains. The BHSI rose 7 points to 646, while the 7TC average increased by $130 to close at $11,623. In both the Continent and Mediterranean, only minimal shifts were seen, with rates marginally firmer than previous levels. Despite limited reported activity, the South Atlantic and U.S. Gulf maintained their firm momentum, with sources noting very tight tonnage availability for February dates.

Meanwhile, Asia continued to face a slow trading pace, with ongoing downward pressure on rates. In the Pacific, the Global Arc (33,438 2013) open Map Ta Phut 9 February was placed on subjects for an Australia round trip in the low $6,000s. The Hai Chang (37,595 2014), open Lumut around 17 February was fixed for an Australia round trip at $8,000, though no further details were disclosed.

BALTIC FORWARD ASSESSMENTS – TUESDAY 10 FEBRUARY 2026 BFA CAPESIZE

PERIOD VALUE CHANGE

Feb 26 22,689 $/day 200

Mar 26 27,468 $/day 661

Apr 26 28,396 $/day 539

May 26 28,964 $/day 535

Jun 26 29,318 $/day 504

Jul 26 29,532 $/day 425

Q1 26 23,861 $/day 287

Q2 26 28,893 $/day 526

Q3 26 29,482 $/day 464

Q4 26 29,654 $/day 458

Q1 27 20,250 $/day 279

Q2 27 25,343 $/day 161

Cal 27 25,829 $/day 315

Cal 28 23,829 $/day 208

Cal 29 21,696 $/day 103

Cal 30 20,661 $/day 40

Cal 31 19,611 $/day 22

BFA PANAMAX 82

PERIOD VALUE CHANGE

Feb 26 15,900 $/day 721

Mar 26 18,414 $/day 889

Apr 26 18,925 $/day 579

May 26 18,811 $/day 579

Jun 26 17,850 $/day 346

Jul 26 17,032 $/day 236

Q1 26 15,873 $/day 537

Q2 26 18,529 $/day 502

Q3 26 16,818 $/day 322

Q4 26 15,857 $/day 296

Q1 27 13,496 $/day 117

Q2 27 15,114 $/day 146

Cal 27 14,525 $/day 232

Cal 28 13,825 $/day 129

Cal 29 13,468 $/day 64

Cal 30 13,107 $/day 11

Cal 31 12,921 $/day 0

BFA SUPRAMAX 63

PERIOD VALUE CHANGE

Feb 26 14,645 $/day 286

Mar 26 17,809 $/day 396

Apr 26 18,755 $/day 460

May 26 18,491 $/day 403

Jun 26 18,152 $/day 393

Jul 26 17,295 $/day 318

Q1 26 15,053 $/day 228

Q2 26 18,466 $/day 419

Q3 26 17,252 $/day 539

Q4 26 16,305 $/day 421

Q1 27 14,291 $/day 146

Q2 27 15,609 $/day 146

Cal 27 14,927 $/day 214

Cal 28 14,545 $/day 100

Cal 29 14,277 $/day 54

Cal 30 14,002 $/day 25

Cal 31 13,941 $/day 7

BFA SUPRAMAX 58

PERIOD VALUE CHANGE

Feb 26 12,611 $/day 286

Mar 26 15,775 $/day 396

Apr 26 16,721 $/day 460

May 26 16,457 $/day 403

Jun 26 16,118 $/day 393

Jul 26 15,261 $/day 318

Q1 26 13,019 $/day 228

Q2 26 16,432 $/day 419

Q3 26 15,218 $/day 539

Q4 26 14,271 $/day 421

Q1 27 12,257 $/day 146

Q2 27 13,575 $/day 146

Cal 27 12,893 $/day 214

Cal 28 12,511 $/day 100

Cal 29 12,243 $/day 54

Cal 30 11,968 $/day 25

Cal 31 11,907 $/day 7

BFA HANDYSIZE

PERIOD VALUE CHANGE

Feb 26 11,765 $/day 130

Mar 26 14,050 $/day 215

Apr 26 14,285 $/day 310

May 26 14,105 $/day 190

Jun 26 13,830 $/day 215

Jul 26 13,555 $/day 225

Q1 26 12,262 $/day 115

Q2 26 14,073 $/day 238

Q3 26 13,175 $/day 130

Q4 26 12,620 $/day 115

Q1 27 11,510 $/day 55

Q2 27 12,200 $/day 20

Cal 27 12,185 $/day 205

Cal 28 11,665 $/day 60

Cal 29 11,435 $/day 70

Cal 30 11,325 $/day 5

Cal 31 11,290 $/day 5

Baltic Exchange Index – 10 FEBRUARY 2025 Baltic Exchange Capesize Index 2771 (- 62)

Route Description Value($) Change

====== =================================== ======== ======

C2 170000mt Tubarao to Rotterdam 11.644 – 0.300

C3 170000mt Tubarao to Qingdao 22.350 – 0.636

C5 160-170000 mt W Australia to Qingdao 7.944 – 0.123

C7 160000mt Bolivar to Rotterdam 15.139 + 0.126 C8_182 182000mt Gibraltar-Hamburg T/A RV 32,550 + 437

C9_182 182000mt Cont/Med Trip China/Japan 51,861 – 306 C10_182 182000mt China/Japan T/P RV 18,955 – 750 C14_182 182000mt China-Brazil or W.Africa RV 25,041 – 1245 C16_182 182000mt Far East – Atlantic BH 6,950 – 139 C17 170000mt Saldanha Bay to Qingdao 16.490 – 0.468

========================================== ======== ========

5TC Weighted Timecharter Average 21,625 – 564 5TC_182 Weighted Timecharter Average 25,128 – 564

Baltic Exchange Panamax 82500mt Index 10 FEBRUARY 2025 Baltic Exchange Panamax Index 1,670 (+ 22)

Route Description Value ($) Change

====== ================================= ======== ====== P1A_82 Skaw-Gib T/A RV 14,809 + 32

P2A_82 Skaw-Gib trip HK-SKorea incl Taiwan 21,909 + 109 P3A_82 HK-SKorea incl Taiwan, Pacific/RV 14,253 + 315 P4_82 HK-SKorea incl Taiwan to Skaw-Gib 8,834 + 212 P6_82 Dely Spore Atlantic RV 15,624 + 264

====== ================================= ======= =====

P5TC Weighted Timecharter Average 15,027 + 198

The following routes do not contribute to the BPI or Weighted TC Average.

Route Description Value ($) Change

====== ================================= ======== ====== P5_82 S. China Indo RV 10,525 + 36

P7 66000mt Mississippi Rvr to Qingdao 52.507 + 0.093 P8 66000mt Santos to Qingdao 39.393 + 0.507

Baltic Exchange Supramax Index – 10 FEBRUARY 2026 Baltic Exchange Supramax Index 1123 (+ 9)

Route Description Value ($) Change

====== ========================================= =========

S1B_63 Cnkle trip via Med or Blsea to China-S.Korea 16,133 + 116 S1C_63 US Gulf trip to China-South Japan 27,250 + 864 BS2_63 North China one Australian or Pacific RV 12,156 – 213 BS3_63 North China trip to West Africa 10,380 + 30

S4A_63 US Gulf trip to Skaw-Passero 28,129 + 1490 S4B_63 Skaw-Passero trip to US Gulf 10,879 + 40

BS5_63 West Africa trip via ECSA to North China 19,700 + 79

BS8_63 South China trip via Indo to EC.India 11,414 – 143

BS9_63 W.Africa trip via ECSA to Skaw-Passero 16,068 + 68

S10_63 S.China trip via Indonesia to South China 8,881 – 119

S15_63 Indian Ocean trip via S.Africa to Far East 12,333 + 25

====== ========================================= =========

| S11TC Weighted Timecharter Average | 14,200 + 123 |

| S10TC Supramax(58) Timecharter Average | 12,166 + 123 |

| Baltic Exchange Index – 10 FEBRUARY 2026 Baltic Exchange Handysize Index 646 (+ 7) |

Route Description Value ($) Change

====== ======================================== =========

HS1_38 Skaw-Passero trip Recalada – Rio de Janeiro 7,264 + 64 HS2_38 Skaw-Passero trip Boston – Galveston 8,836 + 220 HS3_38 Rio de Janeiro-Recalada trip Skaw – Passero 20,094 + 622 HS4_38 USGulf trip via USG or NCSA to Skaw-Passero 19,593 + 950 HS5_38 SE Asia trip to Spore – Japan 9,550 – 300

HS6_38 N.China-S.Kor-Jpn trip to N.China-S.Kor-Jp 9,331 – 150 HS7_38 N.China-S.Kor-Jpn trip to SE Asia 8,731 – 88

====== ======================================== =========

7TC Weighted Timecharter Average 11,623 + 130

(c) Baltic Exchange Information Services Ltd., 2026

Marex Media

The Author

All Rights Reserved “Disclaimer”

All Rights in material and information in this document is reserved. Any form of reproduction or distribution of the information contained in this by any means whether electronic or otherwise is expressly prohibited including distribution by re-producing it anywhere.

I do not guarantee the adequacy, accuracy, timeliness, and/or completeness of the Data or any component thereof or any communication (written, oral, electronic, or other format). The writer shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive, or consequential damages (including but not limited to, loss of profits, trading losses, and loss of goodwill).

The data provided here is sourced from various news media, bulletins and reports from various sources to which I do not have any claim.

Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management or other decision.

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables, images in this Publication, at your own risk or consequences and is only for your personal use.