Global Rankings and Maritime Implications

- The diplomatic push comes as world leaders head to the United Nations in New York for high-level talks. One noticeable absentee is Palestinian President Mahmoud Abbas, who was denied a visa by the U.S. and will now address the U.N. via video link. The US President continue to maintain that he stopped 7 wars in the world.

- Maha Nassar, a scholar of modern Palestinian history at the University of Arizona, lays out the decades long struggle for statehood. She notes that recognition by major Western nations is an important diplomatic moment − more than three-quarters of the world now recognizes a Palestinian state. But that in itself doesn’t make statehood likely so long as the U.S., which opposes statehood at this point, has a veto on the U.N.’s main decision- making body, the Security Council.

- “In fact,” writes Nassar, “many Palestinians and other critics of the status quo say Western nations are using the issue of Palestinian statehood to absolve them from the far more challenging diplomatic task of holding Israel accountable for what a U.N. body just described as a genocide in Gaza.”

· A Great Lakes oil pipeline faces 3

controversies with no speedy resolutions

For more than a decade, controversy over an oil pipeline that passes directly through a Native American reservation and then across a sensitive waterway that is also a key shipping lane has brewed in Wisconsin and Michigan.

Since taking office in January 2025, the Trump administration has joined an already complex fray, with policy decisions and legal filings as well as administrative and judicial appointments that have shifted the strategies and potential outcomes of the situation. The changes affect not just pipeline operator Enbridge but also the environmental, Indigenous and political leaders working to shut down the pipeline, known as Line 5.

Part of the dispute is slated to come before the U.S. Supreme Court in the coming months, but that will not deliver the final resolution of the situation.

Built in 1953, Enbridge’s Line 5 oil pipeline carries petroleum products mostly from western Canada’s tar sands to refineries in eastern Canada, using the Great Lakes as a shortcut. It traverses 645 miles (1,040 km) through Wisconsin and Michigan and transports approximately 23 million gallons of oil and natural gas liquids per day from Superior, Wisconsin, to Marysville, Michigan, and then across the Saint Clair River to Sarnia, Ontario.

The pipeline has been the subject of intense scrutiny since soon after a 2010 oil spill into the Kalamazoo River in Michigan from another Enbridge pipeline with a similar start and endpoint. The 2012 publication of Sunken Hazard, a report from the National Wildlife Federation about the potential for a spill from Line

5, fomented public concern and launched an advocacy

movement that began with questions about Line 5’s safety and has

led to calls for its complete shutdown.

- Donald Trump was more optimistic about Ukraine’s prospects, saying it could reclaim all territory lost in its war with Russia with help from the EU. He also said NATO should shoot down Russian aircraft violating the alliance’s airspace. Volodymyr Zelenskiy told Fox News he thought Trump’s remarks were a big shift.

· The H-1B price tag: How higher fees will reshape tech hiring

India was the largest beneficiary of H-1B visas, accounting for 71% of the 399,395 visas issued in 2024. However, with the sharp increase in fees, the fate of around 400,000 Indian IT professionals, whose H-1B visas may not be renewed, has become a pressing concern.

· Vast source of Rare Earth metal Niobium was dragged to the surface when a supercontinent tore apart

Potentially the largest known source of niobium discovered in central Australia formed 830 million years ago, and we can thank the breakup of the ancient supercontinent Rodinia.

A recently discovered enormous source of niobium — a metal that’s essential for much of today’s technology — appears to have formed when the supercontinent Rodinia ripped apart around 830 million years ago, according to a new study.

The niobium-rich carbonatites, which could be one of the world’s largest sources of the metal, have come from deep within the Earth’s mantle, scientists reported in a study published Sept. 2 in the journal Geological Magazine.

Niobium is a silvery, corrosion-resistant metal

with superconducting properties, making it key for strengthening steel and for use in devices such as MRI scanners and particle accelerators.

Currently, 90% of the global supply of niobium is extracted from a single mine in Brazil, with the other 10% coming from a Canadian mine. Understanding how, where and when these

massive Australian sources formed can help to find new deposits, study co-author Maximilian Dröllner, a sedimentology researcher at the University of Göttingen in Germany, told Live Science.

Although small amounts of niobium can be found encased in various types of rock, the quantities required for economic and

industrial extraction are primarily sourced from carbonatites —

crystalline rocks that consist mainly of magmatic carbonate. Carbonatites are “a bit like a treasure box,” Dröllner said, because they harbour important metal resources and rare earth

elements encased within minerals, Their exact compositions vary depending on where the magma originated inside Earth.

Carbonatites are generally only found beneath Earth’s surface. But because the surface doesn’t reveal what’s buried deep below, exploratory drilling and core extraction are the only ways to know for sure. The two new niobium-rich deposits in Australia’s Aileron Province — called Luni and Crean — were unearthed during such campaigns by the mining companies WA1 Resources Ltd. in 2022 and Encounter Resources in 2023. The Luni deposit has an estimated 200 million metric tons of niobium, and the smaller Crean deposit has around 3.5 million metric tons.

The companies used diamond core drills to extract long, cylindrical sections of material from each site. Dröllner and his team then took eight samples from three Luni drill cores and two samples from a single Crean drill core.

- Trump is Shutting Down the War on Cancer. America’s cancer research system, which has helped save millions of lives, is under threat in one of its most productive moments.

- Trump is expanding the National Guard’s role. Some Former Generals worry. Responding to crises at home is part of the Guard’s mission. Helping crack down on crime in U.S. cities isn’t, say some former leaders, who fear this shift could hurt the force.

- Hit by Trump’s veto power, Nippon Steel reverses US Plant plan. Administration’s ‘golden share’ blocks US Steel’s post- merger restructuring

- The Trump administration has blocked a plan by Nippon Steel to halt the operation of a U.S. Steel plant, invoking its “golden share” in the American steelmaker to intervene.

- Gold price surge leaves Mongolia’s miners in the dust Legal digging by ‘ninjas’ blocked by standoffs with citizens’ councils wary of pollution risks.

The price of gold has never been higher but many observers believe it could rise further given jitters around the U.S. Federal Reserve, import tariffs and resurgent inflation.

· U.S. Defence Secretary Pete Hegseth held his first conversation with his Chinese counterpart and stressed that the United States does not seek conflict with China, but will protect its vital interests in the Asia-Pacific region, the Pentagon said on Wednesday.

- China is Washington’s main geopolitical rival and Hegseth

angered Beijing in May when he urged regional allies to spend more on defence after warning of the “real and potentially imminent” threat from China.

- Pentagon spokesperson Sean Parnell said Hegseth and Chinese Defence Minister Admiral Dong Jun held their “candid and constructive” call on Tuesday.

- “Secretary Hegseth made clear that the United States does not seek conflict with China nor is it pursuing regime change or strangulation of the PRC (People’s Republic of China),” he said.

- “At the same time, however, he forthrightly relayed that the U.S. has vital interests in the Asia-Pacific, the priority theater, and will resolutely protect those interests.”

- Parnell said the two agreed to additional discussions.

- U.S. President Donald Trump has ordered the Department of Defence to rename itself the Department of War, a change that will require action by Congress. The new name would apply to Hegseth as well, altering his title to “Secretary of War.”

- The talks followed a major military parade last week at which

Chinese leader Xi Jinping hosted Russian President Vladimir Putin and North Korean leader Kim Jong Un, sparking concern among some world leaders that they were bearing witness to an important geopolitical shift, although some experts question this.

- Trump responded by saying that Xi, Putin and Kim were conspiring against him. A U.S. official said Trump was “disappointed to see some countries siding with the Chinese” and that “America is going to re-evaluate” the situation.

- China’s state-run news agency Xinhua said Tuesday’s video call

was held at Hegseth’s request. It said Dong urged Hegseth to maintain communication and an open attitude, and to foster stable and positive military ties based on “equal respect, peaceful coexistence, and mutual respect.”

- Xinhua also cited Dong as saying China was committed to working

with regional countries to maintain peace and stability in the South China Sea, a strategic waterway where China and other states have rival claims, and opposes “the infringement and provocation

of certain countries and the deliberate incitement of countries not in the region.”

- The State Department said U.S. Secretary of State Marco Rubio

also spoke on Wednesday with Chinese Foreign Minister Wang Yi in a follow-up to their meeting in Malaysia in July and “emphasized the importance of open and constructive communication on a range of bilateral issues.”

- The July meeting was described by both sides at the time as positive and constructive, despite tension over Trump’s global tariff offensive, in which China has been a major target.

In August, Washington and Beijing extended a partial truce for 90 days, staving off even higher duties, but on Tuesday Trump urged EU officials to hit China with tariffs of up to 100% as part of a strategy to pressure Putin over the war in Ukraine, according to a

U.S. official and an EU diplomat.

- Hamas pens letter to Trump asking for 60- day Gaza truce in exchange for half of hostages – Netanyahu says upcoming year will be a time of

struggle to destroy Iranian axis. IDF officer moderately hurt by Hamas fire in Gaza Monday morning, gunmen killed.

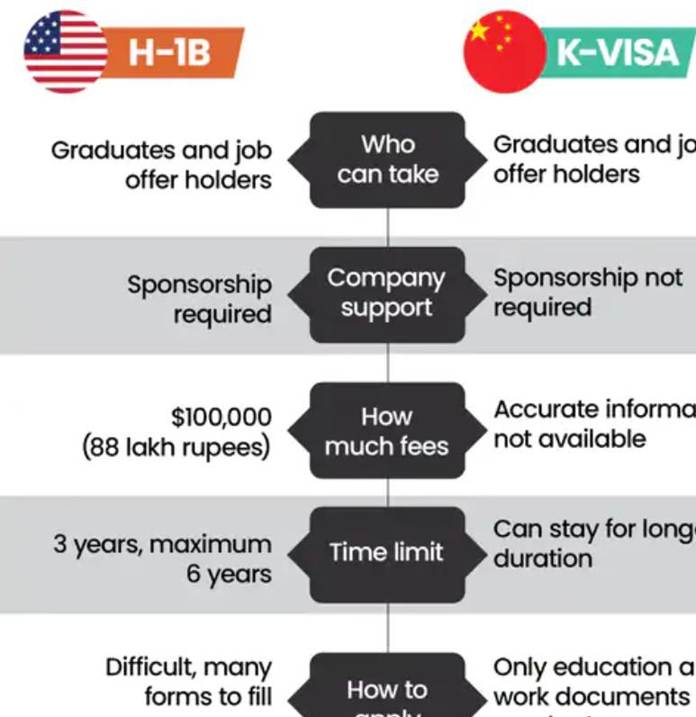

· China launches K visa as Trump hikes H1- B visa fees: Applicants can apply without a Chinese company job offer; UK considers scrapping visa fees

US has increased the H-1B visa fee for professionals from around ₹6 lakh to nearly ₹88 lakh. Meanwhile, China has announced the launch of a new ‘K visa.’

According to the South China Morning Post, the K visa is meant for young people and skilled professionals in the fields of Science, Technology, Engineering, and Math (STEM). It will be issued starting 1 October 2025.

Candidates conducting research in these subjects will also be eligible to apply for the K-visa. The notable part is that applicants will be able to apply even without a job offer from a Chinese company.

The US raised the H-1B visa fee on 21 September, which will make it harder for professionals to move there. In this context, China’s K visa is being seen as an alternative to the H-1B.

UK may scrap ₹90,000 fee

Meanwhile, the UK is also considering abolishing visa fees for highly skilled individuals. According to a Reuters report, those who have studied at one of the world’s top 5 universities or have won a major international award will have their entire visa fee waived.

Currently, the application fee for the UK’s Global Talent Visa is ₹90,000. The UK is set to present its budget on 26 November, and it may decide to scrap this fee before then.

· Trump’s $100,000 Visa Fee Knocks Down Bridge Between

India and the U.S.

The H-1B visa lured a generation of Indian professionals to take part in the American dream. A $100,000 fee has forced a rethink of the route.

- Rachel Reeves could raise £6 billion in income tax without hurting employees by targeting pensioners, landlords and the self- employed, the Resolution Foundation said. It would make Reeves the first British chancellor to increase the basic income tax rate in 50 years.

· Trump Issues Warning Based on Unproven Link Between Tylenol and Autism

Top U.S. health officials urged pregnant women not to use acetaminophen, the active ingredient in Tylenol, claiming it could cause autism, though studies have been inconclusive.

· Why tier II cities matter for Investors.

India’s organised wealth market is just 15% compared to 65% globally — leaving huge room to grow. With HNIs rising in tier II cities, PMS gaining traction, and consolidation underway, the wealth management industry may be small today but is gearing up for explosive expansion.

- Argentina cuts grains export duties to zero to bring in dollars Announced the week after the Central Bank was forced to sell over a billion dollars to defend the peso, the measure will last until October 31, five days after the national mid-terms. Argentina will slash export duties on all grains to zero until October 31, Presidential Spokesman Manuel Adorni announced on Monday morning. The move aims to bring in a stream of dollars at a moment when the financial authorities are haemorrhaging international reserves to stabilize the peso.

A government source and exporters have confirmed to the Herald that the measure includes products in the soy complex. Adorni added on Monday afternoon that export duties on beef and poultry would also be eliminated.

Last week, the Central Bank sold US$1.1 billion over three days to defend the value of the peso after it reached the upper limit of the currency bands. President Javier Milei’s government has blamed the currency run on market fears that the opposition could perform well in the upcoming national legislative elections. Milei has also faced several legislative defeats on public spending in recent weeks.

However, economists have pointed out that the government’s decisions have also worried markets, including their decision not to buy dollars when they were in a position to do so.

“The old politics seeks to generate uncertainty in order to sabotage the government’s program. In doing so, they punish Argentinians: we will not allow it,” Adorni wrote on X on Monday morning. “That is why, with the goal of increasing the supply of dollars during this

period, until October 31 there will be zero export duties on all

grains.”

That date is five days after Argentina’s national mid-term elections, in which half of the lower house and a third of the upper house will be renewed.

At the start of the year, the government announced a temporary cut in export duties. The rates were briefly restored in late June, but

Milei announced a “permanent” reduction a month later.

Cutting export duties to zero means the government is temporarily foregoing a significant source of tax income in order to incentivize exports that will bring in dollars.

The rural sector has said that the national 2026 budget presented last week implies the government is not planning further cuts to export duties, since the budget contains forecasts that income from export duty will rise by 23% next year.

- U.S. tariffs hit 1933 highs; full impact still unfolding

- Global growth seen slowing to 3.2% in 2025, 2.9% in 2026

- U.S. growth to ease to 1.8% in 2025, 1.5% in 2026

-U.S. employers are facing a $14bn annual bill for hiring skilled foreign workers after Trump slapped a $100,000 fee on the cost of securing a visa for new employees to enter the country.

- The OECD warned that the world economy has yet to feel the fullimpact of Donald Trump’s tariffs, but it’s coming, with the US economy set to slow next year. And as his levies curtail Chinese manufacturers’ access to the US market, they are flooding the rest of the world with exports. That’s causing alarm in Latin America and other regions, as governments ponder the potential damage totheir domestic industries.

- AI companies will need $2 trillion in combined annual revenue by 2030 to fund computing power, but their revenue is likely to fall

$800 billion short, according to Bain & Co. That raises further questions about the AI industry’s valuations and business model. China is another threat. Its national champion Huawei unveiled a three-year campaign to overtake Nvidia in AI chips.

· Vogemann linked to six Kamsarmaxes at Hengli Heavy

German shipowner Vogemann has reportedly returned to China for another round of bulk carrier Newbuildings, with reports linking the Hamburg-based company to a fresh series of Kamsarmax orders at Hengli Heavy Industries in Dalian.

Ship market sources suggest Vogemann has committed to six 82,000 dwt vessels at the yard, with deliveries lined up for 2027 and 2028.

Pricing is estimated at around $35m per ship.

The move would extend Vogemann’s already sizeable programme at Hengli, where it has previously ordered both Kamsarmax and Capesize bulkers. The owner has also diversified with Handysize tonnage placed at other Chinese builders.

If confirmed, the new deal will lift Vogemann’s Kamsarmax series at Hengli to 10 ships, strengthening its position among European owners active at the former STX Dalian yard.

· Itochu returns to New Dayang for fresh ultramax pair

Japan’s Itochu Corp has returned to China’s New Dayang Shipyard with

an order for two more ultramax bulk carriers.

The trading house has booked two 64,500 dwt vessels at the Jiangsu yard, part of the state-run Sumec Group, although the price and delivery dates have not been disclosed.

The deal lifts Itochu’s Ultramax orderbook at New Dayang to four, following its order for a pair of ships in April 2024 for handover in 2026 and 2027.

Itochu is the latest Japanese owner to add to its tally at New Dayang. Earlier this year, Kasuga Shipping returned for a second round of orders, bringing its Ultramax series at the yard to five. Kasuga became the shipyard’s first Japanese client with a three-ship deal in early 2024, paying about $34m apiece for 2026 delivery.

· Asso.subsea contracts trenching support newbuild at China Merchants shipyard

Greek offshore contractor Asso.subsea has signed a deal with China Merchants Heavy Industry’s Shenzhen yard for the construction of a new trenching support vessel (TSV).

Named Avra, the vessel, due for delivery at the end of 2027, is being billed as the most powerful purpose-built TSV to date, with 24 MW of installed hybrid power and more than 180 tonnes of bollard pull.

The newbuild is designed primarily for trenching operations in floating wind and subsea cable markets but will also be equipped for cable laying and repair work, the company said. It will be fit to operate two trenching vehicles at once, even in harsh weather, a capability the owner said will speed up project execution and improve reliability.

The ship will carry a 4,000-tonne underdeck cable carousel, twin working decks, a 150-tonne offshore crane and dual A-frames to support a broad range of subsea energy tasks. The design is methanol- and biofuel- ready, fitted with battery hybrid systems and cold-ironing to cut emissions.

The order follows Asso.subsea’s earlier fleet investment in the new

cable layer Althea for delivery also in 2027.

“The contract signing for the construction of the Avra is a strategic milestone,” said Ioannis Togias, executive director of marine technology at Asso.subsea, adding that the vessel has been designed to give the company’s clients “a clear advantage in efficiency and project execution.”

· Seatrium offloads US shipyard to Karpowership

Singapore shipyard group Seatrium has sold its AmMFELS yard located at Brownsville, Texas, for a consideration of S$65m ($50.6m) to Karpower Valley, a related party of Karpowership.

Seatrium stated that the accretive divestment would allow the company to enhance capital and operational efficiencies while unlocking value from one of its surplus facilities.

Following the sale, Seatrium will transition its strategic presence in the US to focus on engineering innovation and technology capabilities through its technology centres and offices located in Houston and a service centre in Mississippi.

The consideration shall be satisfied in cash, of which S$50m ($38.95m) is deferred and to be paid one year after closing. The book value of the divested assets as of June 30, 2025, sold on an “as is, where is” basis, is approximately S$39m ($30.4m).

The completion of the divestment is subject to customary closing conditions, including the transfer of the lease to the new owner by the Port of Brownsville. The Singapore firm said it remains committed to completing all ongoing projects at the yard by the end of 2025.

“Notwithstanding the divestment, the US market remains important to us. We will continue to leverage our global footprint and integrated One Seatrium Delivery Model to deliver world-class solutions to our US- based and global customers in the offshore and energy sectors,” said Chris Ong, CEO of Seatrium.

· Bulker crew stranded in Nigeria without pay for three months

The crew of the 2008-built bulker Eleen Armonia has been stranded in Nigeria for more than three months without receiving salaries.

According to an email sent to Splash from a crew representative, many crew contracts have already expired, but the owner of the Liberian- flagged vessel has refused to arrange repatriation or crew change. He also noted that the crew’s mental health is at a critical level.

Despite repeated complaints filed with the Liberian Registry, the Nigerian Maritime Union, and the vessel’s P&I insurer, no action has been taken.

“The crew remains onboard in increasingly difficult conditions, without income and with uncertainty about when they will be paid or allowed to return home,” the email said.

The Equasis database states that the 55,522 dwt Eleen Armonia is owned and managed by Bulgaria-based Eleen Marine.

“We have been abandoned without wages since June 2025. Our families are suffering, and we have no clear information about when this situation will end. We urgently call on the Liberian flag, the Nigerian authorities, and international organisations to intervene,” the crew representative said.

The crew requests urgent international attention and calls on the Liberian Registry, ITF, and the Nigerian Port State Control to ensure payment of outstanding wages and safe repatriation.

The email stated that this situation may constitute a violation of the Maritime Labour Convention, which guarantees the timely payment of wages and repatriation of seafarers.

· China dominates annual port productivity survey

Container port performance across the world declined between 2020 and 2024 due to the Red Sea Crisis, challenges at the Panama Canal, and pandemic-related shocks, according to a new 79-page report

released by the World Bank Group and S&P Global. However, efficiency gains varied by region and income level.

The report, Container Port Performance Index (CPPI), shows that East Asian ports demonstrated improved performance and led the rankings in 2024. South Asian ports also saw remarkable recovery over the past year, while ports in North America and Europe showcased resilience by maintaining scores close to 2023.

The annual report, which is in its fifth edition, sheds light on emerging trends in port efficiency between 2020 and 2024.

The world’s largest ports in high-income countries were not the only ones to see improvements. Several developing country ports saw noteworthy improvements to their scores and rankings, between 2020- 2024, including Dakar, Jawarharlal Nehru, Mersin, Port Said, and Posorja in Ecuador.

“Even amid the multiple shocks, developing country ports are finding ways to adapt, improve, and maximize value,” said Nicolas Peltier- Thiberge, global director for transport at the World Bank. “It’s a reminder that with better planning, technology, and cooperation across the logistics chain, ports can make significant strides in their efficiency.”

This edition of the CPPI offers a global benchmark of 403 container ports worldwide, utilising a dataset that includes more than 175,000 vessel calls and 247m container moves with a focus on total vessel time in port

“As we navigate an increasingly complex global shipping environment, understanding and improving port performance is essential for economic growth and competitiveness,” said Turloch Mooney, global head of port intelligence and analytics at S&P Global Market Intelligence.

Of the top 20 performing ports in 2024, 10 are in China.

· CMA CGM expands UK footprint with Freightliner takeover

France’s CMA CGM has moved to strengthen its European intermodal offering with the acquisition of Freightliner UK Intermodal Logistics, one of Britain’s largest rail freight operators.

The deal covers Freightliner’s rail and road operations, inland terminals

and the Freightliner brand itself. The acquisition is expected to close in

early 2026, subject to regulatory approvals. Other Freightliner operations in continental Europe – Heavy Haul, Rotterdam Rail Feeding, and activities in Poland and Germany – will remain under existing ownership.

Freightliner UK will continue as a multi-user, multi-customer business, run independently by its current teams, while gaining access to CMA CGM’s global logistics and shipping network, the French liner giant said.

For CMA CGM, the move underlines its strategy to expand sustainable and competitive transport options in Europe. By pairing maritime strength with inland rail capability, the French shipping group said it aims to push further into end-to-end logistics solutions.

“Acquiring Freightliner strengthens our intermodal presence in the United Kingdom, a strategic market for CMA CGM,” said Rodolphe Saadé, chairman and CEO, adding: “It allows us to connect sea, rail and road more efficiently, delivering better solutions for our customers while expanding lower-carbon transport options.”

Rail freight has become a central pillar of supply chain decarbonisation in Europe. By enabling shippers to switch from road to rail, the industry can cut CO₂ emissions significantly. CMA CGM said the deal would accelerate that shift by combining Freightliner’s operational know-how with its own global logistics reach.

The company noted that with Freightliner’s rail network, it can better link the UK’s hinterland to Europe’s major ports, offering customers greater flexibility and reduced emissions.

CMA CGM already has a strong base in the UK. Its UK agency operates 28 services linking the country to the rest of the world, moving more than 800,000 teu last year. Through subsidiary CCIS, the group also moved 200,000 teu by rail and road between January and July 2025.

· Oman is rapidly becoming a hub for Russian shipping

- Over 30 ships previously registered to Russian entities have moved to Oman so far this year

- Vessels previously owned by Sovcomflot, Fesco, JS Volga Shipping and Prime Shipping are now Muscat-registered

- Tightening compliance scrutiny from Dubai authorities are creating opportunities for Oman, which is growing trade ties with Russia

· Cost of green hydrogen rears its ugly head

- Rollout of hydrogen-based green fuels would require ‘staggering’

amount of power

- IMO rules must be strong enough to catalyse broader investment

- Carbon capture problems complicate the case for e-methanol and e-methane

- If the IMO sets its rewards right, e-fuels producers could tap billions in subsidies. But the huge costs make that uncertain.

· Ageing feeder fleet demands greater investment despite rise in smaller boxship orders

- Orders for sub-5,000 teu boxships have been rising since the second quarter, but more investment needed to meet demand for larger ships in intra-regional trades

- Feeder segment remains underrepresented in newbuilding orders, risking future supply shortages

- Despite the rise in smaller boxship orders, the orderbook for ships under 5,000 teu represents just 6.5% of existing fleet

- The historic solution of cascading older, larger ships to feeder routes may no longer be viable due to inefficiency and unsuitability.

· John Fredriksen adds four VLCC newbuildings to private fleet in Chinese deal

Seatankers said to have swooped for more vessels at Hengli Heavy that

were previously linked to tycoon’s Frontline company

John Fredriksen has built up his private shipping fleet with a fresh VLCC newbuilding deal in China.

The Norwegian-born shipping tycoon has inked a deal for four firm 306,000-dwt tankers at Hengli Heavy Industries, ships previously linked to his listed Frontline operation.

· ‘Relentless rally’: Red-hot VLCC market here to stay

Shifting trade patterns should sustain VLCC rate levels in the medium to long term, says Breakwave Advisors

Lucrative VLCC freight markets look likely to continue after rates for modern scrubber-fitted ships pushed towards $100,000 per day.

New York’s Breakwave Advisors said the tanker sector is recovering from a prolonged period of staggered rates, as the growth in new vessel supply is shrinking, while oil demand remains elevated in line with the global economy.

“A historically low orderbook combined with favourable shifting trade

patterns should continue to support increased spot rate volatility, which,

combined with the ongoing geopolitical turmoil, should sustain freight

rates in the medium to long term,” the company added.

· MSME steel importers seek govt exemption on paid-for imports as prices rise

MSME steel importers are seeking a government exemption from a new quality control order and BIS approval requirements, arguing the mandate has fuelled a sharp spike in prices and left their businesses in financial jeopardy. A new government quality control order on steel is pitting India’s micro, small, and medium enterprises against regulators, with importers claiming the measure has triggered a sharp rise in domestic prices and supply shortfalls.

In a letter dated 17 September, the Metals and Stainless Steel Merchant’s Association (Massma) has asked the ministry of steel to allow exemptions for shipments for which advance payments were made before the quality control order (QCO) took effect in June.

· Diana Shipping charters out Kamsarmax to NYK Line

Greek bulker owner Diana Shipping has entered into a time charter contract with Nippon Yusen Kabushiki Kaisha (NYK Line) for one of its kamsarmax dry bulk vessels.

The company hired the 2014-built, 82,165 dwt bulker Leonidas P. C. The gross charter rate is $14,000 per day, minus a 5% commission paid to third parties, until a minimum of September 15, 2026, up to a maximum of November 15, 2026.

The charter is expected to commence on September 24, 2025, and generate approximately $4.93m of gross revenue for the minimum scheduled period of the time charter.

Diana Shipping’s fleet consists of 36 dry bulk vessels – four Newcastlemaxes, eight Capesizes, four Post-panamaxes, six Kamsarmaxes, five Panamaxes, and nine Ultramaxes.

The company also expects to take delivery of two methanol dual-fuel newbuilding Kamsarmax bulkers by the second half of 2027 and the first half of 2028, respectively.

Currently, the combined carrying capacity of the fleet, excluding the two vessels not yet delivered, is approximately 4.1m dwt with a weighted average age of 11.83 years.

· Shipping bosses in Singapore call for immigration shake-up

Singapore’s maritime hub status is unquestioned — but its shipping community is increasingly vocal about one factor it believes could undermine future competitiveness: immigration.

From shipmanagers to recruiters, industry leaders argue that Singapore’s ability to attract, retain, and integrate global talent is under strain from rigid policies and red tape. Their message is clear: if the Lion City wants to remain the world’s premier shipping hub, it needs to rethink how it handles foreign professionals.

“Let’s not sugarcoat it — talent is our greatest asset, but also our greatest bottleneck,” says Ryan Kumar, director at recruitment firm Direct Search Global. “We can move a vessel across the globe faster than we can bring in a candidate. Immigration approvals should match the pace of business.”

Kumar calls for “more agility, less red tape” and a sector-specific approach. “A seasoned technical superintendent or chartering manager isn’t growing on trees in Singapore. We need targeted flexibility for sectors facing real shortages. Many of the best people I place come from India, the Philippines, Europe, or the Middle East. They bring deep sector knowledge and commercial instinct. Let’s make Singapore the place where this talent wants to land — and can do so quickly.”

For BSM Singapore managing director Raymond Peter, the solution lies in precision. “A more dynamic Shortage Occupation List would be beneficial for businesses, particularly if it is more precisely defined for niche maritime-specific roles,” he says. “This is especially important in rapidly evolving areas like alternative fuels and maritime digitalisation. A more dynamic list would attract global specialists who are critical for the sector’s transformation.”

Bureau Veritas vice president for Southeast Asia, Drago Pinteric, echoes that call, arguing for a responsive, skills-based framework. “Such a system would enable companies to more efficiently bring in foreign professionals with specialised expertise in advanced technologies, complex supply chains, and emerging fuels – areas where local talent is limited.”

Union Marine Management Services boss Vinay Gupta stresses the importance of stability. “The driver of the maritime industry in Singapore is its human capital — yet the majority operate on employment or work passes, with little focus on long-term sustainability or succession planning,” he says. “A clearer path for expatriates in critical sectors to progress towards permanent residency would go a long way in attracting stronger talent, encouraging knowledge transfer, and ensuring continuity.”

Wilhelmsen Ship Management’s CEO and president, Haakon Lenz, is aligned. “Streamlining long-term employment and PR processes for skilled maritime professionals could help in long-term talent retention,” he says.

Others point to softer factors. Columbia Shipmanagement Asia CEO Demetris Chrysostomou argues that making life easier for families is key. “If we make it easier for families to settle, we make it easier for businesses to stay. Any form of assistance with housing, schooling, and integration would help attract and retain top international talent.”

Consultant Peter Schellenberger looks to Dubai for inspiration. “It is ok to check whether a Singaporean wants the job or is qualified, but otherwise open the doors again backed by contracts. One big other factor would be to give expats access to public schools as many families can’t afford to come.”

The common refrain across the industry is that Singapore risks losing its edge if talent flows slow down. “A country that wins the talent war will win the business game,” Kumar warns. “Right now, we’re still playing defence.”

For a nation that thrives on global shipping, the call from industry insiders is unambiguous: immigration policy must evolve as fast as the industry it serves.

Baltic Reports

BALTIC INDICES 23/09/2025

DRY INDEX: 2200 (+28)

| CAPESIZE | INDEX: | 3469 (+104) |

| PANAMAX | INDEX: | 1799 (-23) |

| SUPRAMAX | INDEX: | 1486 ( 0) |

| HANDYSIZE | INDEX: | 820 (+3) |

BCI TC AVG $/DAY 28770 (+867)

BPI82 TC AVG $/DAY 16190 (-210)

BSI TC AVG $/DAY 18789 (+5)

BHSI TC AVG $/DAY 14757 (+54) TIMECHARTER

‘Nav Vidya’ 2009 83610 dwt dely Gangavaram 24/28 Sep trip via EC India redel China $16,000 – Propel Shipping

‘Yangze 21’ 2012 82122 dwt dely Panjin 26 Sep trip via EC Australia redel Malaysia $14,000

‘Tai Knight’ 2022 82042 dwt dely retro Seki Saki 20 Sep trip via EC Australia redel India $16,000 – Bainbridge Navigation

‘Pacific Bliss’ 2025 81928 dwt dely CJK 25 Sep trip via Vancouver redel N China $16,000 option S China $15,350 – Cobelfret – <Scrubber benefit to Owners>

‘Giewont’ 2010 79649 dwt dely aps EC. S.America 22 Sep trip via Mediterranean redel Passero $26,000.

‘Guo Hai Lian 681’ 2013 75784 dwt dely Mauban 25/29 Sep trip via Indonesia redel S China $16,500 – Tongli

‘Darya Vidya’ 2021 64723 dwt dely Tomakomai 20/25 Sep trip via NoPac redel India $21,000 – Bunge

‘HG Hongkong’ 2010 53743 dwt dely Spore 20 Sep trip via Indonesia redel China $14,000

‘Warrior’ 2024 40053 dwt dely Eemshaven 25/30 Sep trip via Baltic redel Luanda intention grain $19,750 – Fednav

‘Gullholmen Island’ 2011 38309 dwt dely Vitoria prompt trip redel Continent $23,500

PERIOD

‘Leonidas P.C.’ 2011 82165 dwt dely CJK 22 Sep 11/13 months redel worldwide $14,000 – NYK

‘Devbulk Gulten’ 2013 38302 dwt dely Rio Grande 29 Sep/1 Oct 4/6 months redel worldwide $17,150

VOYAGES ORE

‘Ares Venture’ 2008 190000/10 Tubarao/Qingdao 16/20 Oct $24.25 fio 3 days shinc/30000shinc – Oldendorff

‘TBN’ 170000/10 Dampier/Qingdao 7/9 Oct $10.75 fio 90000shinc/30000shinc – Rio Tinto

‘TBN’ 170000/10 Dampier/Qingdao 7/9 Oct $10.65 fio 90000shinc/30000shinc – Rio Tinto

‘TBN’ 160000/10 Port Hedland/Qingdao 9/11 Oct $10.75 fio 80000shinc/30000shinc – BHP

‘TBN’ 160000/10 Port Hedland/Qingdao 7/9 Oct $10.80 fio 80000shinc/30000shinc – FMG

COAL

‘TBN’ 175000/10 Drummond/Icdas 3/12 Oct $17.50 fio scale load/35000shinc – Oldendorff

‘TBN’ 70000/5 Puerto Bolivar/Safi 1/10 Oct $17.15 fio scale/45000shinc – ST Shipping

Baltic Exchange Index – 23 September 2025 Baltic Exchange Capesize 182 Index

Route Description Value Change

===== ===============================================

C8_182 182000mt Gib/Hamburg transatlantic RV 33,300 +2243 C9_182 182000mt Cont-Med trip China-Japan 54,313 +500 C10_182 182000mt China-Japan transpacific RV 32,320 +160 C14_182 182000mt China-Brazil round voyage 30,720 +450 C16_182 182000mt Backhaul 12,113 +132

=======================================================

C5TC 182 Weighted Timecharter Average 32,290 +584

Baltic Exchange Index – 23 September 2025 Baltic Exchange Capesize Index 3469 (+104)

Route Description Value($) Change

====== =================================== =====

| C2 | 160000mt Tubarao to Rotterdam | 12.914 +0.175 |

| C3 | 160-170000mt Tubarao to Qingdao | 25.015 +0.170 |

| C5 | 160-170000mt W Australia to Qingdao | 10.770 0.005 |

| C7 | 150-160000mt Bolivar to Rotterdam | 14.900 +0.636 |

| C8_14 180000mt Gibraltar-Hamburg T/A RV | 29,786 +2429 | |

| C9_14 180000mt Conti/Med Trip China/Japan | 49,644 +581 | |

| C10_14 180000mt China/Japan T/P RV | 29,195 +195 | |

| C14 180000mt China-Brazil RV | 27,000 +505 | |

| C16 180000mt N.China to Skaw-Passero | 8,550 +94 | |

| C17 170000mt Saldanha Bay to Qingdao | 18.891 + 0.119 | |

========================================== ========

5TC Weighted Timecharter Average 28,770 +867

Baltic Exchange Panamax 82500mt Index 23 September 2025 Baltic Exchange Panamax Index 1,799 (- 23)

Route Description Value ($) Change

====== =========================================

| P1A_82 Skaw-Gib T/A RV | 17,836 | -959 |

| P2A_82 Skaw-Gib trip HK-SKorea incl Taiwan | 25,706 | -446 |

| P3A_82 HK-SKorea incl Taiwan, Pacific/RV | 14,769 | +253 |

| P4_82 HK-SKorea incl Taiwan to Skaw-Gib | 8,588 | +97 |

| P6_82 Dely Spore Atlantic RV | 15,364 | +4 |

====== ================================= =======

P5TC Weighted Timecharter Average 16,190 – 210

The following routes do not contribute to the BPI or Weighted TC Average.

Route Description Value ($) Change

====== =======================================

| P5_82 S. China Indo RV | 14,206 +450 |

| P7 66000mt Mississippi Rvr to Qingdao | 56.075 -0.254 |

| P8 66000mt Santos to Qingdao | 38.717 -0.097 |

Baltic Exchange Panamax 82 Asia Index – 23 September 2025

Route Description Size (MT) Value($) Change

===== ==================================

P5_82 S.China one Indo RV 14,206 +450

Baltic Exchange Supramax Index – 23 SEPTEMBER 2025 Baltic Exchange Supramax Index 1486 (0)

Route Description Value ($) Change

| ====== | ========================================= ==== | ||

| S1B_63 | Cnkle trip via Med or Blsea to China-S.Korea 20,854 -29 | ||

| S1C_63 | US Gulf trip to China-South Japan 31,586 +236 | ||

| BS2_63 | North China one Australian or Pacific RV | 16,250 | -207 |

| BS3_63 | North China trip to West Africa | 16,360 | -200 |

| S4A_63 | US Gulf trip to Skaw-Passero | 33,604 | +461 |

| S4B_63 | Skaw-Passero trip to US Gulf | 14,724 | +154 |

| BS5_63 | West Africa trip via ECSA to North China | 22,157 | +107 |

| BS8_63 | South China trip via Indo to EC.India | 18,567 | -246 |

BS9_63 W.Africa trip via ECSA to Skaw-Passero 18,221 +150 S10_63 S.China trip via Indonesia to South China 13,917 -233 S15_63 Indian Ocean trip via S.Africa to Far East 15,592 +367

====== ========================================= ====

S11TC Weighted Timecharter Average 18,789 + 5 S10TC Supramax(58) Timecharter Average 16,755 + 5

Baltic Exchange Supramax Asia Index – 23 September 2025

Route Description Value($) Change

====== =============================== =======

S2_63 N.China one Austr or Pac RV 16,250 -207 S8_63 S.China via Indonesia/Ec India 18,567 -246 S10_63 S.China via Indo/S.China 13,917 -233

====== =============================== =======

S3TC Weighted Time Charter Average 16,245 -226

Baltic Exchange Index – 23 SEPTEMBER 2025 Baltic Exchange Handysize Index 820 (+ 3)

Route Description Value ($) Change

====== ======================================== =====

HS1_38 Skaw-Passero trip Recalada – Rio de Janeiro 9,800 +146 HS2_38 Skaw-Passero trip Boston – Galveston 12,339 +189 HS3_38 Rio de Janeiro-Recalada trip Skaw – Passero 22,778 +95 HS4_38 USGulf trip via USG or NCSA to Skaw-Passero 20,479 +86 HS5_38 SE Asia trip to Spore – Japan 13,775 +46 HS6_38 N.China-S.Kor-Jpn trip to N.China-S.Kor-Jpn 12,814 -61 HS7_38 N.China-S.Kor-Jpn trip to SE Asia 12,650 -69

====== =============================================

7TC Weighted Timecharter Average 14,757 + 54

(c) Baltic Exchange Information Services Ltd., 2025

Marex Media

The Author

Mr Bansi Jaising – photo you have

All Rights Reserved “Disclaimer”

All Rights in material and information in this document is reserved. Any form of reproduction or distribution of the information contained in this by any means whether electronic or otherwise is expressly prohibited including distribution by re- producing it anywhere.

I do not guarantee the adequacy, accuracy, timeliness, and/or completeness of the Data or any component thereof or any communication (written, oral, electronic, or other format). The writer shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive, or consequential damages (including but not limited to, loss of profits, trading losses, and loss of goodwill).

The data provided here is sourced from various news media, bulletins and reports from various sources to which I do not have any claim.

Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management or other decision.

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables, images in this Publication, at your own risk or consequences and is only for your personal use.