Summer is over in the United Kingdom. The end August Bank holiday has passed and, with it, the Notting Hill Carnival. As people return to their desks, we expect a more positive direction in shipping markets after a somewhat directionless holiday period.

In the dry and wet bulk sectors, hopes for better rates and sustained values hinge upon restricted fleet growth over the next one to two years. The demand side is less clear as China’s economy and exports are slowing with the prospect of lower raw material imports that go into making steel, oil products and manufactured goods. One big question is how long the export window remains open for exporting excess steel, petroleum products and electric vehicles to the detriment of those industries in recipient nations.

A US and EU backlash against EVs is already in play. Another may soon ramp up on steel and aluminium. Iron ore prices are down 30% this year and further weakness possibly lies ahead. However, lower prices will marginalise and shut down more expensive second and third tier producers, including many mines in China that produce low-grade ore lacking in ferrous content. This would support the major global producers, especially in Australia and Brazil, as they substitute competing high-price output by exporting more of their product to China and elsewhere.

This year, China is expected to achieve its fifth consecutive year of a billion tons of steel output, thus supporting and maybe increasing China’s imports of high-grade but low-cost iron ore. We understood this week that China National Petroleum Corp, and its listed arm PetroChina, face stagnant output at home and a scarcity of new projects globally to boost reserves even as slowing economic growth and surging EV usage erode domestic demand. We should not write off continued crude oil import demand.

Maybe, it is the area of geopolitics that holds the key to shipping fortunes in 2025.

In Ukraine, Putin was taken by surprise at Ukraine’s recent lightening move into Kursk.

Zelensky wants to improve his negotiating position in the event of peace talks but has shown little interest in ceding territory.

For his part, Putin seeks to take all of Ukraine and is far from achieving this objective. So, peace talks may rumble on, as much as to appease western powers as anything else. Ukraine has only just taken delivery of its first batch of F-16s and is closer to being unshackled on how it can use western weapons.

An eventual truce may ease Black Sea grain exports but western sanctions against Russia’s energy sector should prove enduring, with substitute oil and gas trades having already been put in place. There may be no return to the pre-Feb 2022 status. The western world will continue to largely boycott Russian oil and gas while the energy-hungry likes of India and China will continue buying at discounted prices.

The ton-mile boost to oil and gas seaborne trade may remain in place for a long time.

The Israel-Hamas war grinds on despite the protestations of the US, UK, France, Germany, Egypt, Qatar and others. Israel has pledged to wipe out Hamas, and Hamas has pledged to wipe out Israel, in what appears to be a gladiatorial contest to the bitter end. It may be naïve to expect a two-state solution after October 7, and everything that has followed. A one-state solution, either/or, is more likely. Lately, we have seen a shift of focus to Hezbollah in Lebanon and trouble is also brewing in the West Bank. Two new fronts are unfolding and, once they are eventually ‘resolved’, then Iran itself may represent unfinished business. This promises to be a forever war.

Under the circumstances, it is hard to imagine safe passage to commercial shipping via the Red Sea and Suez Canal any time soon. We have seen owners have their ships run the gauntlet putting steel, cargo and crew at great risk in exchange, presumably, for vastly elevated freight payments.

The current example of the 2006-built 163,800-dwt suezmax tanker, Sounion, shows how the Houthis have total disregard for the environment, ignoring the fact that the shores of Yemen, and the livelihoods of its fishermen, will be the first in line to suffer the consequences of oil pollution.

Most car carriers, container ships and gas carriers are taking the long route round the Cape of Good Hope in passages from east to west, adding 7-14 days to their voyages.

A few owners of bulk carriers and tankers seem to be more willing to take the risk of Red Sea transit although the rising chance of being randomly targeted by the Houthis should make them think twice.

Today, the BCI-5TC settled at $25,700 daily, a decent level, and yet we are still in August. The strength of the capesize segment defies the gloom and doom of a China slowdown and stagnation in its steel and property sectors. In these troubled event-driven times, nothing can be taken for granted.

Dry Cargo Chartering

The upward momentum continued for Capesize markets this week, propped up by a healthy influx of cargoes in the Pacific as well as more notably from Brazil and West Africa.

The Baltic Exchange average freight price ex. South America to China gained around $1.75 pmt this week to end up at $28.00 pmt, and overall time charter averages closed at $25,700, an increase of $2,055.

From Port Hedland, BHP took Amorito (179,322-dwt, 2012) for 160,000 mtons 10% to Qingdao at $11.50 pmt, while FMG fixed the same route at the same price and Panocean covered at $11.00 pmt.

From Dampier, Rio Tinto took three positions and paid from $11.00 pmt to $11.65 pmt.

Half the world away in the Atlantic, Cargill Metals took an Oldendorff TBN for Pointe Noire/China at $31.75 pmt, while Element chartered Nicolemy (179,910-dwt, 2014) for Tubarao/Qingdao at $27.50 pmt, and Mercuria fixed Pan Advance (179,185-dwt, 2009) with the option of loading West Africa or Brazil at $27.00 pmt.

Elsewhere, TKSE covered Seven Islands/Rotterdam at $7.45 pmt, and Trafigura reportedly fixed Cape Friendship (185,879-dwt, 2005) for Narvik/Qingdao at $32.30 pmt.

Another week of downward pressure was seen for Panamax markets.

Overall time charter averages dipped down to $11,843, a decline of $881 since last reported. Some fresh enquiry was seen from Australia and Indonesia resulting in a more positive sentiment there, whilst in the Atlantic we saw rates in the US Gulf slide away and remain relatively flat in South America.

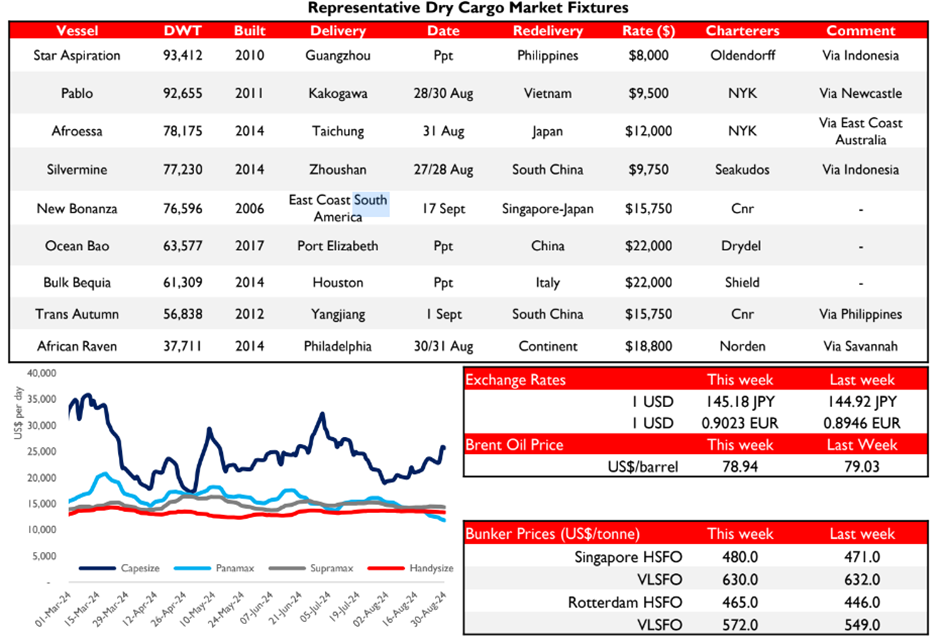

From the Pacific, NYK took Pablo (92,655-dwt, 2011) delivery Kakogawa for a trip via Newcastle to Vietnam at $9,500, Louis Dreyfus fixed Okinawa (81,397-dwt, 2009) delivery Ulsan for a NoPac round trip at $11,000, and Prevail Star (81,055-dwt, 2014) was covered delivery Cigading for a trip via Indonesia to India at $12,500. Additionally, Shandong Xin De (82,000-dwt, 2024) was chartered for 1 year trading delivery ex. yard at $18,500 with scrubber benefit to Charterers and worldwide redelivery.

In the Atlantic, Aquavita Air (82,192-dwt, 2020) fixed aps East Coast South America for a trip to Skaw-Passero at $17,500 to Louis Dreyfus, Pioneer Eternity (80,916-dwt, 2021) also fixed delivery aps East Coast South America but for a fronthaul at $16,250 plus $625,000 bb, and Swissmarine took Treasure Star (82,206-dwt, 2010) delivery US Gulf for a trip to Skaw-Gibraltar range at $15,000 plus $150,000 bb.

The BSI closed at $14,369, down $129 from last week. It was another slow week in the Atlantic, with few fixtures surfacing at similar levels to last done. Bulk Bequia (61,309-dwt, 2014) open Huston was fixed for a trip via US Gulf redelivery Italy with petcoke at $22,000 by Shield, CL Ganjiang (63,500-dwt, 2023) was fixed by Drydel basis delivery Lagos for a prompt trip redelivery China at $20,500.

Meanwhile in the Pacific, the Southeast Asia market dropped further with many prompt vessels ballasting from Bangladesh and open prompt in Singapore, however it seemed that the bottom had been reached coming to the end of the week. More mid-September cargoes came out on Friday.

North Asia was still, with a steady volume of steel and general cargo exports, although north Pacific and Australia remains flat. HTK Mighty (58,612-dwt, 2012) fixed delivery Koh-Sichang for a prompt trip Indonesia redelivery Thailand with coal at $12,000 by Chinaland, while in the north, the market was supported by the backhaul enquiries, BBG Kindness (63,253-dwt, 2015) open Zhoushan was fixed to Hanson for a trip via China to West Coast Central America at $16,500 with a split rate after 65 days.

In the Indian Ocean, Aggelos B (58,479-dwt, 2010) was fixed basis delivery Kandla for a trip redelivery Arabian Gulf at $12,000 by Allianz, Oslo Venture (63,234-dwt, 2015) was fixed to Drydel basis delivery Port Elizabeth prompt for a trip redelivery China at $21,250 plus $212,500 bb.

The Handysize market in the Atlantic was flat this week, with the exception of the US Gulf. The BHSI closed today at $13,387 down $167 from last week.

Activity on the Continent started picking up little by little, giving positive signs for September. Trips from the Continent were recorded around $10,000 per day. Ken Un (37,429-dwt, 2015) open Continent fixed via St Lawrence to West Africa with grains around $18,500 with York Overseas. Mediterranean was lagging a bit behind, with limited fresh enquiry. Operators often choosing to fix in-house tonnage for the few cargoes that entered the market. Intra-Mediterranean trips heard fixed in the 9,000’s per day basis arrival pilot station. Ultrabulk covered their usual stem from East Mediterranean to North Coast South America on a small Handy at low $8,000’s per day.

The US Gulf is the strongest performing market in the Atlantic, Orcinus (34,094-dwt, 2010) heard fixed from Houston to Italy with wheat at TCE high $18,000 with De Cecco. Julia (37,449-dwt 2018) open Port Everglades fixed Texas to West coast Central America with Petcoke at $20,000 with Weco Bulk.

Despite the gains in the US Gulf, South America softened this week, a 37k-dwt was heard fixed at $14,500 Brazil to the Continent.

The Pacific Handy market was subdued this week and the overall sentiment was negative with limited fresh enquiry across Asia and Australia/New Zealand. Earlier this week, bullish owners who held onto their rates from last week, were left short, and realigned to market levels dropping their numbers by the end of the week.

Tonnage lists in both the Far East and South East Asia are also seen to be increasing. In the Far East, a 32k-dwt vessel open North China was heard fixed at around $12,000 levels for a trip to Southeast Asia while another 31k-dwt vessel open Japan was heard fixed at $11,750 for a trip to Southeast Asia. A 40k-dwt vessel open Lanshan was heard fixed around mid $16,500 levels for 2-3 laden legs.

In Southeast Asia, a 28k-dwt vessel open Koh-Sichang was heard fixed at $10,500 levels for an Australia round voyage to the Far East. A 30k-dwt vessel open Campha was heard fixed at low $10,000’s levels for a trip within South East Asia.

Dry Bulk S&P

WEEKLY COMMENTARY

To Lords – the home of English cricket. The less diligent London shipbrokers have spent this morning with one ear tuned to the BBC commentary of the England vs Sri Lanka test match, willing the new wunderkind all-rounder, Gus Atkinson, to his first test century.

With three more sales clipped away this week, the Capesize market is also getting close to its century for the year. A quick scan of the scoreboard records 86 Capers and Newcastlemaxes changing hands so far and at this rate the Capesize market will be raising its bat in salute well before the Christmas decorations are up in the shops.

The sale of the week is the Newcastlemax Cape Azalea (208,025-dwt, 2012 NACKS) to Chinese buyers at $38.5m which is pretty much in line with benchmarks. The older, scrubber-fitted Maran Prosperity (174,240-dwt, 2006 SWS) accepted a firm $21.5m, also from Chinese buyers.

Finally in this busy sector the elderly, out-of-class Lila Lisbon (176,423-dwt, 2003 Universal) is sold for just $12.5m, which represents a 25% premium to scrap. Again, the buyers were Chinese.

Another Dolphin57 is snapped up.

Sania (57,011-dwt, 2010 Qingshan) is sold at $12.5m – which is pretty much par for her age and pedigree.

For the Handysizes, the modern Japanese-built logger African Egret (34,370-dwt, 2016 Namura) is sold at $21.5m while the smaller Ince Evrenye (28,207-dwt, 2013 Imabari) received $12.7m. Both sales are as per benchmarks.

Reported Dry Bulk Sales

Vessel DWT Built Yard Gear Buyer Price Comment

Cape Azalea 208,025 2012 NACKS Chinese $38.5m

Lila Lisbon 176,423 2003 Universal Chinese $12.5m Non-IACS & Surveys overdue

Maran Prosperity 174,240 2006 SWS Chinese $21.5m Scrubber fitted

Sania 57,011 2010 Qingshan C 4 x 30T Chinese $12.5m

Isolda 34,941 1999 Mitsui C 3 x 30T $5.1m Lakes fitted

African Egret 34,370 2016 Namura C 4 x 30T $21.5m

Ince Evrenye 28,207 2013 Imabari C 4 x 31T $12.7m

Tanker Commentary

MR tankers take the spotlight in this week’s short sales list. Although not concluded yet, Scorpio’s STI Opera (49,990-dwt, 2014 HMD) is understood to be closely negotiating closely in the low $42m which is firm against the last sister ship sold in June, with Great Eastern picking up STI Beryl (49,990-dwt, 2014 HMD) for $36.6m. Both units have electronic main engines and good docking positions.

Values for non-eco tonnage remain healthy, as Fos Power (47,371-dwt, 2007 Onomichi) has secured a price of $24m. The strong price achieved on the Fos Power could perhaps be an indicator that the discount typically seen for pumproom ships, like the Fos Power, compared to deepwell units is starting to narrow, which may not be a surprise in such a heated second-hand market.

A comparison with the two years younger Nave Orbit (49,999 2009 SPP) which sold for $26.0m last month may hint at this trend. That said, the Fos Power is also a notable step up on the previous pumproom sale – Daytona (47,407-dwt, 2005 Onomichi) at $18m in July, and the Nave Orbit did have surveys due too. This discount is something to keep an eye on in the coming weeks.

Meanwhile, Kalamos (46,719-dwt, 2004 Iwagi) has gone for $17.8m which is also firm for a ship of this age given her surveys are due, however she is Zinc coated which will have carried a premium with the right buyer.

Have a good weekend (long one in the US due to Labour Day)

© Pure Ventures

Marex Media