- UK braces for snow as temperatures tumble from 22C to single digits.

- Double Trouble for the US: Two key reports released Thursday showed the US economy may be in a state of early-onset stagflation — a toxic one-two punch of slow economic growth and rising prices.

That’s a particularly problematic combo because slow economic growth should, in normal times, drag prices down, not up. It’s Econ 101: When people are out of work or worried about losing their jobs, they spend less, spurring businesses to lower prices. If people can’t afford things but prices go up anyway, that’s a sign something is deeply broken.

Consumer prices rose 0.4% in August, driving the annualized inflation rate to 2.9% — the highest since January. That was up from 2.7% in July. At the same time, first-time applications for unemployment benefits surged last week to their highest level in four years. An estimated 263,000 people filed initial unemployment insurance in the week ended September 6, according to Department of Labor data released Thursday.

“The whiff of stagflation is getting stronger,” Harvard economics professor Jason Furman wrote on Bluesky Thursday. “There are no good options for the Fed given the set of circumstances we’re facing.”

- Fitch boosts India’s FY26 GDP outlook to 6.9% from 6.5% estimated in March 2026, citing stronger than expected momentum in the services sector and resilient consumption spending from both households and government.

- Rise in U.S. Inflation Likely to Keep Fed Cautious on Pace of Rate Cuts

- The Consumer Price Index rose 2.9 percent compared with the same time last year, the fastest annual pace since the start of 2025.

- India explores rare-earth deal with Mynamar rebels. India is working to obtain rare-earth samples from Myanmar with the help of a powerful rebel group, as it seeks alternative supplies of a strategic resource tightly controlled by China. India asked state- owned and private firms to explore collecting and transporting samples from mines in north eastern Myanmar that are under Kachin Independence Army’s control.

- Coking coal imports to jump 42% by 2030 on Steel demand. India’s coking coal imports are expected to rise nearly 42% to 115 mio tonnes by the end of the decade, driving by surging demand from the Steel sector, according to a report prepared by Ernst Young Parthenon and the Indian Steel Association.

- The EU will significantly ramp up sanctions against Russia and its enablers after the violation of Polish airspace by Russian

drones. Poland got offers of support for its air defense, Prime Minister Donald Tusk said.

- France’s new Prime Minister Sebastien Lecornu is seen by colleagues as savvy and cordial, earning praise from even Marine Le Pen in private—a reputation that gives him a fighting chance to garner support for his budget plans.

· China’s latest probe targets: senior diplomat, financial specialist

This week’s China Up Close focuses on two senior officials who have become the latest probe targets. Liu Jianchao — the head of the Chinese Communist Party’s International Department who was supposed to accompany North Korea’s Kim Jong Un and other foreign leaders at events related to the Sept. 3 military parade — was not seen during the extravaganza. Three days later, Chinese authorities announced that Yi Huiman, former chairman of the China Securities Regulatory Commission, had been placed under investigation for “serious violations of discipline and law.”

The two are members of the party’s Central Committee, which will hold its fourth plenary session next month. Before Liu and Yi apparently fell out of favour, there was a spate of purges, including within the military. Attention is now focused on how the key session will reshuffle personnel.

- Dubai’s Housing Boom Is Stoking Fears of Another Crash

- The city is experiencing record home sales, but some observers worry about a 2009 repeat.

- Alex Zagrebelny is constructing Eywa, a 21-story residential tower in Dubai, with design elements inspired by the Avatar movies and Vastu Shastra.

- The Dubai real estate market has been booming since 2020, with some observers wondering if it is a bubble ready to burst, while others point to stringent lending rules and maturing market regulation.

- Critics note that the market has lured many new developers, with nearly a quarter of a million homes on track for completion in the next few years, which could represent a 30% increase in the supply of housing in Dubai, according to Jones Lang LaSalle Inc.

- All this sounds Pollyanna-ish when France is in a full-blown political crisis. President Emmanuel Macron has appointed his defence minister, Sebastien Lecornu, as his fourth prime minister in less than two years. With a seemingly intractable fiscal problem, the cost of insuring French debt has risen with each step in the political turmoil:

With widespread street protests by a group called Bloquons Tout (“Let’s Block Everything”), successors to 2018’s gilets jaunes, and France’s legislature split between three roughly equal but incompatible political blocs, Lecornu’s chances of finding a meaningful fiscal resolution look minimal. And yet the negativity might create an opportunity. Since the beginning of 2024, French stocks have lagged the rest of the

continent by 12%.

· Crude Reality

Oil seems ever less sensitive to geopolitical shocks. In the last week, it’s barely reacted to two major flashpoints: Israel’s strikes deep inside US ally Qatar, risking dangerous escalation in the Middle East, and Russia’s brazen violation of Polish airspace, the Kremlin’s most direct engagement with NATO in recent times. It prompted Poland to invoke NATO’s Article IV, which calls for mutual defence.

After the Polish incident, oil rose as much as 2.3% before giving up some of the advance. Brent crude remains below its 100-day and 200-day moving averages. Bloomberg Economics’ Dina Esfandiary and Ziad Daoud argue that although the temporary spike is understandable, prices are no more likely to rise persistently after this latest strike than after other recent flashpoints in the Middle East. Qatar is a significant gas provider, but its production and transportation facilities remain intact:

- There are several lessons Europe and the US should take away from Russia’s unprecedented decision to send drones into Poland as part of another Kremlin attack on Ukraine.

One is that nobody should ever again dismiss the idea that Russia— struggling so mightily in Ukraine—would ever take on a North Atlantic Treaty Organization member. It just did, Champion writes. Nineteen drones entered Polish airspace, according to Foreign Minister Radek Sikorski, enough to make clear it was deliberate and for Poland to invoke NATO’s Article 4, calling on allies to consult when a member is under threat.

European leaders told the Associated Press they believe the

incursion was an intentional expansion of Russia’s war on Ukraine rather than being a mistake. “Russia’s war is escalating, not ending,” European Union foreign policy chief Kaja Kallas told the AP. “What Putin wants to do is to test us. What happened in Poland is a game-changer.”

Champion says the overnight incursion over one of NATO’s best-armed member states also shows the corrosive effect of Europe’s military incapacity and America’s lack of political will. The combination has allowed Russia to seize the initiative in Ukraine this year. This drone manoeuver, was just a warning shot.

· Troim sights US listing for VLCC owner backed by Livanos, Lauro and two former Frontline chief executives

- Growth project for Bruton will start with newbuildings and seek multiple capital raises to fund expansion in rising market

- Tor Olav Troim is planning to take a VLCC fleet to the US capital markets in a move backed by a host of star-studded shipping names. His Oslo-listed company Bruton is looking to combine its two-strong VLCC newbuilding fleet with two other big tanker newbuildings from a parallel private project, Andes Tankers, in a major escalation of his ambitions in the sector.

- Troim is working with shipping heavyweights Peter Livanos, Emanuele Lauro and Niels Stolt-Nielsen on the project.

· Clasen Rickmers-led Asian Spirit Steamships expands into dry bulk sector

German feeder container company has bought one Chinese-built handysize bulk carrier from Nisshin Shipping

Container ship owner Asian Spirit Steamship Co (ASSC) has entered the the dry bulk sector by acquiring a secondhand handysize vessel.

The Clasen Rickmers-led company has emerged as the owner of the Jiangmen Nanyang-built 39,300-dwt bulker NY Trader III (built 2016), which it has renamed Spirit of Tokyo.

· Blaze-hit Wan Hai container ship finds refuge in UAE port

Vessel was earlier rejected by Sri Lankan port authorities.

A fire-damaged Wan Hai container ship has finally found a port of refuge, four months after it suffered an under-deck explosion off the coast of Kerala in south-west India. DP World and the Dubai Ports Authority have given approval for the 4,333-teu Wan Hai 503 (built 2005) to berth at Jebel Ali, the UAE’s largest container port.

· Dubai ship manager blacklisted in biggest US sanctions package yet against Houthis

Four tankers placed on blacklist for operating at Ras Isa port The Trump administration has blacklisted a Dubai ship

management company and four tankers as part of the biggest US sanctions package yet targeting the Houthis. The US Treasury Department added 32 people and entities to its sanctions list for being part of networks facilitating the Yemeni militant group, which is backed by Tehran. Among those targeted was the United Arab Emirates’ Tyba Ship Management and its owner, Muhammad Al- Sunaydar, who is accused of being a Houthi-linked businessman.

· Good news for VLCCs as Frontline chief argues rogue oil producers are hitting their peaks

Russia, Iran and Venezuela are being pushed out by Atlantic producers, Frontline CEO says. Forget sanctions squeezing oil exports out of Russia, Iran and Venezuela — Frontline chief executive Lars Barstad believes those countries are nearing peak production. The head of the John Fredriksen-backed tanker owner said the three countries need investment to keep the oil flowing, which could be a tough task, given the sanctions and increasing crude coming out of the Atlantic basin and all helping to boost VLCCs.

“We were very deeply surprised by the fact that Iran and Venezuela were able to actually ramp up exports over the last couple of years, particularly Iran, being the most sanctioned country in the world,” Barstad said during Pareto Securities’ Energy Conference in Oslo on Thursday.

· Ammonia as fuel ‘not a fairytale’, Exmar says as first newbuilding hits water

Company unveils raft of floating ammonia solutions

Exmar will take delivery of a pioneering ammonia dual-fuel midsize gas carrier newbuilding in the first quarter of 2026. Speaking at Gastech in Milan, director of fleet operations & technical business development Kristof Coppe said the ship is launched, and sea trials on the first of four 46,000-cbm ammonia carrier newbuildings will start this year.

The vessel, which has been designed with two 500-cbm deck tanks and is fitted with a WinGD ammonia dual-fuel engine, will start sea trials with diesel, and at the beginning of 2026 will go on gas trials with ammonia.

· China Cosco Shipping mulls multibillion- dollar orders for 100 vessels

- Domestic shipyards have reserved berths for bulkers, tankers, container ships, MPPs and semi-submersibles

- China Cosco Shipping is embarking on a multibillion-dollar newbuilding order spree that would expand its enormous orderbook, already worth more than $18bn.

- Several shipbuilding players said the shipping giant, which has almost 180 newbuildings of various ship types on order, has reserved more than 100 berths at domestic shipyards.

- The fresh expansion and renewal drive at the world’s largest shipowner comes as Beijing has been calling on shipowners to rejuvenate their domestic and international fleets.

· Investors in offshore vessel companies want cash not ships, Pareto analyst says

Newbuildings will make money, but investors do not want to see more capacity, Jorgen Sovik Opheim argues.

Offshore vessel newbuildings will make money, but investors still want cash, Securities analyst Jorgen Sovik Opheim opined.

· ![]() Shipping’s fuel transition hits a supply-side reality check

Shipping’s fuel transition hits a supply-side reality check

Nearly as many alternative-fuel ships are on order as in service, according to data carried in the latest Maritime Forecast to 2050 report from DNV.

By 2030, the global fleet will have the capacity to consume over 50m tonnes of oil equivalent of low-greenhouse gas emitting fuels, the report forecasts. This figure is double the estimated volume needed to meet the International Maritime Organization’s (IMO) 2030 emissions target. Yet today, actual consumption of low-GHG fuels remains at just 1m tonnes.

“This widening gap between capacity and use highlights both the scale of industry commitment and the urgent need for fuel producers and infrastructure developers to accelerate supply to match the fleet’s readiness,” the report states.

With the number of alternative-fuelled vessels in operation set to almost double by 2028, shipping is approaching what DNV claims

is a “fuel transition tipping point” – sending a strong demand signal to fuel producers and related industries to speed up their progress.

“The industry has made real technical progress in recent years,” said Eirik Ovrum, lead author of the 73-page report. “But these solutions are still operating in silos. To deliver impact, they need to be integrated into fleet strategies, supported by infrastructure, and recognised in compliance frameworks. That’s where the next phase of work must focus.”

· Korea Shipowners’ Association hits out at POSCO’s HMM takeover plans

The Korea Shipowners’ Association has hit out at reports the country’s top steel mill is being linked with taking over national flagship, HMM.

Advisors from Samil PwC and Boston Consulting Group have been working with POSCO on feasibility studies for a deal that could be worth in the region of KRW7trn ($5bn), covering the combined 71.7% stake held by state creditors. State-run Korea Development Bank has been sounding out potential suitors for years. Hyundai Glovis, LX Pantos, and SM Line have all been linked, but none have gained traction. Back in 2021, POSCO’s name was also in the frame, though the then mooted price tag was barely a quarter of today’s.

South Korea’s shipowners’ association issued a statement today,

saying HMM — rebuilt at huge taxpayer expense — could

“degenerate into a subsidiary for POSCO’s in-house cargo transport” rather than competing with global containerlines. The fear is that if POSCO’s core steel business falters, HMM could again be sacrificed, undoing years of restructuring under the government’s five-year shipping reconstruction plan.

The association flagged three specific risks: first, that container shipping — a highly specialised global business — would suffer from non-professional management; second, that POSCO could use HMM primarily for its own cargo, squeezing out domestic rivals; and third, that this would “collapse the foundation of Korea’s shipping industry” and harm exporters. Shipowners pointed to POSCO’s failed venture with Geoyang Shipping as evidence of the risks of industrial carriers trying to run shipping lines. They also cited Brazil’s Vale as another cautionary tale.

· CMA CGM rules out surcharge ahead of US fees on Chinese tonnage

France’s CMA CGM, the world’s third-largest containerline, has told clients it is fully prepared for next month’s hiked port fees in the US for Chinese-linked tonnage, and that it does not envisage implementing surcharges because of the new ruling.

In April, the US Trade Representative detailed plans to start charging China-linked tonnage calling at US ports from the October 14 this year, in a bid to both curb China’s dominance in the field of shipbuilding as well as boost domestic shipyard capabilities. The final rules remain unpublished. Customs & Border Protection is working on a collection system. CMA CGM said yesterday it has been rejigging its fleet to ensure it will be ready for the new rules, telling clients: “Despite the challenges this new service fee may create for our operations, based on the current structure and applicability of the service fee, CMA CGM does not plan to implement a surcharge at this time to cover USTR-related fees as currently structured.”

Some of CMA CGM’s partners in the Ocean Alliance – COSCO and OOCL – face greater hurdles come October 14 with transport analysts at HSBC recently suggesting the two Chinese carriers could face a combined bill of more than $2.1bn in 2026. Maersk, meanwhile, has publicly stated it will look to avoid putting any

Chinese-built ships onto the US trade, something it expects its competitors to follow suit.

Global shipping, not just the container sector, is realigning fleets in anticipation of October’s extra port fees to be levied by the US on China-linked tonnage. This is already being reflected in chartering decisions for transatlantic tanker and dry bulk fixtures with Chinese-built tonnage shifting to other parts of the globe.

· Saipem wins $1.5bn deal for offshore gas development in Turkey

Italian energy services major Saipem has been awarded a new offshore contract by Turkish Petroleum for the third phase of the Sakarya gas field development project.

Sakarya is the largest offshore natural gas field discovered in Turkey, located approximately 170 km off the coast of Filyos. The third phase of development entails a new dedicated FPU, fed by 27 wells located in the Sakarya and Amasra fields.

Saipem’s scope of the $1.5bn contract includes the EPCI of eight rigid flowlines and a 24-inch diameter gas export pipeline, approximately 183 km long, connecting the offshore field at a maximum depth of 2,200 m.

The overall duration of the contract is approximately three years, while the offshore campaign will be conducted by Saipem’s Castorone pipelay vessel in 2027. Saipem has completed the first phase of the Sakarya field development project awarded in 2021 and is finalising activities related to the second phase awarded in 2023.

· DNV maritime boss highlights ‘major concern’ with IMO net zero framework

‘Roadblocks’ in the LNG pathway, Orbeck-Nilssen told reporters Calls for clarity on how the net zero fund will come back to shipping.

Low GHG fuels will be scarce, so continued focus on other decarbonisation methods will be required to hit IMO targets

After its Maritime Forecast to 2050 report laid bare the size of the mountain shipping must climb to hit its decarbonisation targets, DNV maritime chief executive Knut Orbeck-Nilssen called for pragmatism to prevail

Mozambique joins rapidly growing fake flag roster for sanctioned tonnage | Cargo insurance premiums ‘dropping off cliff,’ IUMI said Iron ore may face demand question for the first time in decades.

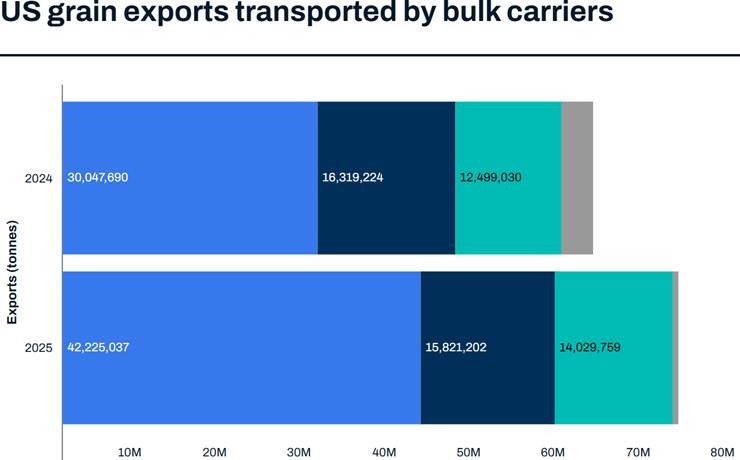

· Bulker fallout looms as trade tensions threaten US soyabean season

US bulk grain volumes in January-August rose 16% year on year, driven by a surge in corn shipments, but the trend could reverse in September-December. Soyabeans have an outsized effect on US export volumes; as the soyabean export season begins, China remains out of the market Unreliable and uncertain US trade policy could accelerate a long-term shift towards South American producers. US grain exports outperformed through August, but are poised for a fall in the final four months of the year as China continues to boycott American soyabeans.

THE INITIAL effect of Trump 2.0 trade policies has been far more negative for US businesses than for global ship operators. The broader fallout for shipping is not here yet, but could arrive soon.

On the container side, US businesses have been hammered with over $100bn in new import levies to date, yet containerised import volumes in the first eight months of 2025 increased 3% year on year (y/y), largely due to first-half frontloading. Pressure on US container shipping demand is expected to come with a lag, at the back end of this year and into 2026. There’s a similar delayed pattern on the dry bulk front, for a different reason.

China has an overall tariff rate of 34% on US soyabeans, according to the American Soybean Association. US agricultural sales to China have collapsed. According to cargo inspection data from the US Department of Agriculture, US grain loadings aboard bulkers bound for China have largely ceased since late April.

Nevertheless, total US grain exports in January-August were up double digits y/y due to booming shipments of corn to non-Chinese buyers.

The lag effect on the US-China trade conflict on dry bulk is the result of crop seasonality. The brunt of consequences will come in the next several months, during the US soyabean export season.

“The tariffs have had a limited impact on soyabeans to this point as they occurred outside the major export window. That is quickly changing,” warned the ASA in a new white paper.

China frontloaded cargoes from South America this year to prepare for the absence of US cargoes in 2025-2026, posting record soyabean imports in May-August.

“China currently has zero new crop export orders for US soyabeans for 2025-2026,” said the ASA. Other buyers have not picked up the slack, with new crop sales down 81% from the five- year average. “The bottom line is that if China doesn’t come back this season, we will lose business,” said Jay O’Neil of HJ O’Neil Commodity Consulting in an interview with Lloyd’s List.

That would be a negative for Panamax rates, particularly given the earlier pull-forward in South American cargoes to China.

“The dry bulk industry may look at this January to August and say we’re okay. Well, not necessarily, because the real negative demand effect could happen in the next few months, assuming that the US and China don’t come to terms,” said O’Neil.

Corn cargoes boost export volumes through August.

The USDA cargo inspection data highlights how positive US exports have been for bulker demand in the first eight months of this year. US grain exports in January-August totalled 90.2m tonnes, up 14% y/y. Of this year’s volumes, 80% was shipped aboard bulkers, 16% went by rail or truck to Mexico, and 4% was containerised (primarily soyabeans).

US grain export volumes shipped aboard bulkers totalled 72.7m tonnes, up 16% y/y. This equated to around 1.2m tonnes of additional bulker cargoes per month versus the same period in 2024.

Bulk corn volumes surged to 42.2m tonnes in January-August, up 41% y/y, with bulk wheat cargoes reaching 14m tonnes, up 12% y/y.

Bulk soyabean volumes fell by just under 500,000 tonnes, or 3% y/y, to

15.8m tonnes, as declines to China during the off-season were offset by other buyers.

January-August bulk volumes of other grains fell by 3.2m tonnes due to a plunge in Chinese buying of US sorghum that was not offset elsewhere, according to the USDA inspection data.

US bulk grain shipments to China plunged by 63% or 10.1m tonnes y/y in the first eight months of 2025. Bulk soyabean volumes fell by 38%.

The inspection data showed no US corn or wheat cargoes aboard China-bound bulkers (although there have been shipments of containerised corn), and an almost complete loss of sorghum volumes.

The 3.7m tonne y/y decline in bulk soyabean shipments to China was offset by gains to Mexico, Japan and Colombia, as well as higher volumes to elsewhere in Latin America, and to Europe and Asia.

The 1.2m tonne y/y decline of bulk corn shipments to China was more than offset by much higher buying elsewhere, led by South Korea (up 3.3m tonnes y/y), Japan (up 1.3m tonnes), Colombia (up 812,032 tonnes) and Mexico (up 374,365 tonnes).

“We’re missing a major buyer — China — and not just for soyabeans but for all grain commodities,” said O’Neil. “But corn has been terrific for exports. The biggest reason is Mexico and the second biggest reason is Japan.”

In terms of total volumes (including bulker, container and truck/rail shipments), Mexico is by far the largest buyer of US grain exports. Japan is a distant second.

A caveat for bulker demand is that recent upside from higher volumes has been partially offset by shorter distances, as long-haul voyages to China have been replaced by shorter-haul moves to Mexico, Colombia and other Latin American buyers such as Guatemala and the Dominican Republic.

Another negative for dry bulk shipping demand, related to Mexico, is the rising use of rail as Mexico grows in importance as a buyer.

US grain volumes to Mexico shipped by land (almost all rail, plus some trucking) in January-August totalled 14.2m tonnes — more than the entire volume shipped by ocean to number-two Japan.

Rail volumes accounted for 65% of Mexican grain imports from the US in the first eight months of this year, and were up 431,277 tonnes y/y.

‘Dire’ situation for US soyabean exports

US farmers are already suffering under Trump 2.0 due to a combination of falling crop commodity prices, higher costs for fertilisers and machinery, and labour constraints due to the immigration crackdown.

It’s about to get worse for American farmers. The outlook for 2025-2026 soyabean exports is increasingly ominous, spurring the ASA to plead with US president Donald Trump for relief.

“US soyabean farmers are standing at a trade and financial precipice,” wrote the ASA in a letter to Trump, calling the farmers’ situation “dire” and warning that they “cannot survive a prolonged trade dispute with our largest customer”. US trade talks with China are scheduled to extend until mid-November. In a normal year, peak export volumes of US soyabeans load in October.

“The further into the autumn we get without reaching an agreement with China on soyabeans, the worse the impacts will be on US farmers,” said the ASA. The next few months will have an outsized impact on total US grain exports for the year, and consequently, for Panamax bulker demand. A steep drop-off in US soyabean loadings in the months ahead could offset some of the y/y gains from corn through August.

China accounted for 60% of US soyabean export volumes transported via bulkers in full-year 2024. US bulk soyabean exports to all destinations in the final four months of 2024 accounted for 25% of full- year bulk exports of all grain commodities, according to USDA data.

“This is the time of year when the sun shines, when we make hay, and if China doesn’t come back in, we miss that window of opportunity,” said O’Neil. “We will gain some export business from other countries that Brazil won’t have extra capacity to supply, but it would be a net loss for exports.”

Longer-term concerns for US farm exports

The longer-term concern of US farmers, beyond the current soyabean marketing season, is that trade tensions and tariffs could increasingly push buyers away from the US — to Brazil, in particular.

In contrast, dry bulk executives view a shift towards South America and away from the US as generally positive for freight rates.

The voyage from Santos, Brazil to Shanghai is twice as long as from the US Pacific Northwest to Shanghai, and slightly longer than from the US Gulf to Shanghai via the Panama Canal (albeit shorter than the Cape of Good Hope route from the US Gulf to Shanghai). In addition, South American grain ports are much more prone to congestion than US ports, which decreases effective vessel supply.

“The tariffs are not simply doing temporary damage. They’re doing permanent damage,”.

He noted that the pitch of US agricultural sector has long been: The US is a reliable buyer, unlike South America, which has more interruptions in exports.

“But the tariffs are sending a message that we’re no longer a reliable buyer, and that’s going to encourage further expansion in Brazil, the Black Sea and other areas, and it’s going to motivate our foreign buyers, not just China but also other countries, to diversify to a greater degree than they already have.

“My fear, personally, is that we’re not just hurting soyabean exports for 2025-2026, but we’re probably doing damage to corn and soyabean exports for decades.”

· TEN inks third VLCC newbuild amid ‘strong’ market fundamentals

Confirmation of third 320,000 dwt vessel at Hanwa Ocean accompanied by disclosure of option for a fourth unit. New York-listed owner of 82 vessels on the water and on order has $3.7bn in contracted revenues.

Second-quarter net income falls due to lower charter rates and lack of vessel sale windfalls.

Baltic Reports 11th September, 2025 BALTIC INDICES 11/09/2025

DRY INDEX: 2111 (- 1)

| CAPESIZE | INDEX: | 3041 (-30) |

| PANAMAX | INDEX: | 1998 (+23) |

| SUPRAMAX | INDEX: | 1484 (+ 6) |

| HANDYSIZE | INDEX: | 801 (+ 3) |

BCI TC AVG $/DAY 25218 (- 247) BPI82 TC AVG $/DAY 17983 (+ 205) BSI TC AVG $/DAY 18755 (+ 78) BHSI TC AVG $/DAY 14419 (+ 55)

TIMECHARTER

‘Tramontana’ 2011 93246 dwt dely Mariveles 15/16 Sep trip via Indonesia redel SE Asia $14,750 – D’Amico

‘Thunder Island’ 2021 82558 dwt dely Bahudopi 20

Sep trip via N Australia redel Singapore-Japan intention iron ore $15,750 + $100,000bb

‘New Ascent’ 2012 82179 dwt dely Onahama 3 Sep trip via NoPac redel Singapore-Japan $16,500

‘Alpha Discovery’ 2016 82057 dwt dely Caofeidian 16 Sep trip via East Australia redel South China intention coal $14,000

‘Pu An Tong’ 2012 81649 dwt dely CJK 13 Sep trip via Indonesia redel South Korea $12,500 – GNS

‘Ornak’ 2010 79677 dwt dely Liuheng 13/16 Sep trip

via North Pacific redel Singapore-Japan intention grains

$13,200 – Cargill

‘Skopelos I’ 2011 79659 dwt dely Lianyungang 12/14 Sep trip via E Australia redel S China intention coal

$13,000 – Dooyang

‘Lemessos Wind’ 2009 76523 dwt dely Hong Kong 14/15 Sep trip via Indonesia redel Japan $14,500 option redel China $15,500 – Cargill

‘Cetus Narwhal’ 2016 43482 dwt dely SW Pass prompt trip redel NC South America $18,000 – Contilines

‘Vecco’ 2015 38850 dwt dely Beaumont prompt trip redel Aratu intention sulphur $17,250 – Bainbridge

‘CS Calvina’ 2011 37456 dwt dely SW Pass prompt redel NC South America intention grains $18,000 –

Clipper

‘Clarabelle’ 2014 37423 dwt dely SW Pass prompt trip redel Algeria intention grains $19,500 – Pangaea

‘Clipper Alexandria’ 2010 32535 dwt dely Yantai 11 Sep trip redel WC India intention fertilisers $15,250

PERIOD

‘Tai Kinship’ 2021 84509 dwt dely passing Singapore 10 Sep 4/6 months redel worldwide $18,000 – Cobelfret

‘Minorca’ 2023 81157 dwt dely Qingdao 15/20 Sep 5/7 months redel worldwide $16,000

VOYAGES ORE

‘Cape Britannia ‘ 2009 170000/10 Port Hedland/Dangjin 28/30 Sep $10.35 fio 95000shinc/45000shinc – Glovis

‘TBN’ 170000/10 Dampier/Qingdao 27/29 Sep $10.30 fio 90000shinc/30000shinc –

Rio Tinto

‘Bulk Harvest ‘ 2012 160000/10 Port Hedland/Qingdao 25/29 Sep $10.55 fio 80000shinc/30000shinc – NYK

‘TBN ‘ 160000/10 Port Hedland/Qingdao 27/29 Sep $10.60 fio 80000shinc/30000shinc – Mercuria

COAL

‘TBN ‘ 150000/10 Samarinda/Mundra 15/21 Sep $7.00 fio 15000shinc/40000shinc

– LSS

‘Hanaro TBN’ 80000/10 Gladstone/Dangjin 30 Sep/4 Oct $13.27 fio 35000satpmshexuu/22500shinc – Kepco

Baltic Exchange Index – 11 SEPTEMBER 2025 Baltic Exchange Capesize 182 Index

Route Description Value Change

===== ========================================== ====

C8_182 182000mt Gib/Hamburg transatlantic RV 28,086 + 93 C9_182 182000mt Cont-Med trip China-Japan 49,288 – 187 C10_182 182000mt China-Japan transpacific RV 29,862 – 1328 C14_182 182000mt China-Brazil round voyage 27,761 – 844 C16_182 182000mt Backhaul 11,050 + 2619

=================================================== ====

C5TC 182 Weighted Timecharter Average 29,147 – 358

Baltic Exchange Index – 11 SEPTEMBER 2025 Baltic Exchange Capesize Index 3041 (- 30)

Route Description Value($) Change

====== =================================== ======

| C2 | 160000mt Tubarao to Rotterdam | 12.321 + 0.528 |

| C3 | 160-170000mt Tubarao to Qingdao | 23.710 – 0.380 |

| C5 | 160-170000mt W Australia to Qingdao | 10.295 – 0.295 |

| C7 | 150-160000mt Bolivar to Rotterdam | 13.486 – 0.064 |

C8_14 180000mt Gibraltar-Hamburg T/A RV 24,494 + 29 C9_14 180000mt Conti/Med Trip China/Japan 44,494 – 100 C10_14 180000mt China/Japan T/P RV 26,620 – 1425 C14 180000mt China-Brazil RV 24,050 – 825

C16 180000mt N.China to Skaw-Passero 7,425 + 2569 C17 170000mt Saldanha Bay to Qingdao 18.006 – 0.255

========================================== =======

5TC Weighted Timecharter Average 25,218 – 247

Baltic Exchange Panamax 82500mt Index 11 SEPTEMBER 2025 Baltic Exchange Panamax Index 1,998 (+ 23)

Route Description Value ($) Change

====== ================================= ======== P1A_82 Skaw-Gib T/A RV 22,577 + 682

P2A_82 Skaw-Gib trip HK-SKorea incl Taiwan 28,571 + 240 P3A_82 HK-SKorea incl Taiwan, Pacific/RV 14,459 + 229 P4_82 HK-SKorea incl Taiwan to Skaw-Gib 8,550 + 69 P6_82 Dely Spore Atlantic RV 16,709 – 180

====== ================================= =======

P5TC Weighted Timecharter Average 17,983 + 205

The following routes do not contribute to the BPI or Weighted TC Average. Route Description Value ($) Change

====== ================================= ======== P5_82 S. China Indo RV 13,804 +254

P7 66000mt Mississippi Rvr to Qingdao 57,850 + 0.186 P8 66000mt Santos to Qingdao 40,543 – 0.014

Baltic Exchange Supramax Index – 11 SEPTEMBER 2025 Baltic Exchange Supramax Index 1484 (+ 6)

Route Description Value ($) Change

====== ========================================= =====

S1B_63 Cnkle trip via Med or Blsea to China-S.Korea 19,908 + 191 S1C_63 US Gulf trip to China-South Japan 30,871 + 457 BS2_63 North China one Australian or Pacific RV 16,936 + 107 BS3_63 North China trip to West Africa 16,750 – 70 S4A_63 US Gulf trip to Skaw-Passero 31,507 + 228 S4B_63 Skaw-Passero trip to US Gulf 14,214 – 50 BS5_63 West Africa trip via ECSA to North China 21,379 + 172 BS8_63 South China trip via Indo to EC.India 19,850 – 58 BS9_63 W.Africa trip via ECSA to Skaw-Passero 17,836 + 97

S10_63 S.China trip via Indonesia to South China 15,286 – 93

S15_63 Indian Ocean trip via S.Africa to Far East 14,583 + 175

====== ========================================= ======

S11TC Weighted Timecharter Average 18,755 + 78 S10TC Supramax(58) Timecharter Average 16,721 + 78

Baltic Exchange Index – 11 SEPTEMBER 2025 Baltic Exchange Handysize Index 801 (+ 3)

Route Description Value ($) Change

====== ======================================== =========

HS1_38 Skaw-Passero trip Recalada – Rio de Janeiro 9,157 + 114 HS2_38 Skaw-Passero trip Boston – Galveston 11,564 + 128 HS3_38 Rio de Janeiro-Recalada trip Skaw – Passero 21,211 + 283 HS4_38 USGulf trip via USG or NCSA to Skaw-Passero 20,136 – 64 HS5_38 SE Asia trip to Spore – Japan 13,829 0

HS6_38 N.China-S.Kor-Jpn trip to N.China-S.Kor-Jpn 13,000 0 HS7_38 N.China-S.Kor-Jpn trip to SE Asia 12,950 – 25

====== ======================================== =========

7TC Weighted Timecharter Average 14,419 + 55

(c) Baltic Exchange Information Services Ltd., 2025

Marex Media

The Author

Mr Bansi Jaising

All Rights Reserved “Disclaimer”

All Rights in material and information in this document is reserved. Any form of reproduction or distribution of the information contained in this by any means whether electronic or otherwise is expressly prohibited including distribution by re- producing it anywhere.

I do not guarantee the adequacy, accuracy, timeliness, and/or completeness of the Data or any component thereof or any communication (written, oral, electronic, or other format). The writer shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive, or consequential damages (including but not limited to, loss of profits, trading losses, and loss of goodwill).

The data provided here is sourced from various news media, bulletins and reports from various sources to which I do not have any claim.

Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management or other decision.

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables, images in this Publication, at your own risk or consequences and is only for your personal use. ++