- Ship Manager (V. Ships) Pleaded Guilty of Marine Pollution, Fined $ 2 Million

- V.Ships Norway A.S. pleaded guilty today to violating the Act to Prevent Pollution from Ships and was sentenced to pay a $2 million fine. V.Ships admitted that oily bilge water and oily waste was discharged from the M/T Swift Winchester and the discharges were omitted from the Oil Record Book.

- “Dumping oil-contaminated waste into the waters around our ports and coasts violates the law and poses an unnecessary health and environmental hazard,” said Acting Assistant Attorney General Adam Gustafson of the Justice Department’s Environment and Natural Resources Division (ENRD). “The crew took pains to hide their illegal activity by knowingly keeping inaccurate records. We will not turn a blind eye to this kind of irresponsible and fraudulent activity.”

- “The Gulf of America and the Texas ports are amazing places with great natural beauty. They are also vital to our economy,” said Acting U.S. Attorney Jay R. Combs for the Eastern District of Texas. “When a foreign ship operated by a foreign company discharges polluting wastes, it threatens waters that are vital to the United States and the state of Texas. We will hold those responsible for polluting the Gulf of America accountable.”

- “The criminal prosecution of this case underlines our commitment to enforcing the Act to Prevent Pollution from Ships” said Acting U.S. Attorney Ellison C. Travis for the Middle District of Louisiana. “The illegal discharge of bilge water and oily waste from vessels poses a significant threat to our waters and marine life and by holding those accountable who violate these standards, we send a clear message that we will not tolerate actions that endanger our environment. We remain dedicated to ensuring that the maritime industry operates responsibly and in compliance with environmental laws.”

- Coast Guard Marine Inspectors, Pollution Responders and Investigating Officers undergo rigorous and specialized training to detect and gather evidence of environmental crimes. This expertise alongside our federal partnerships was crucial to the successful

prosecution of this violation,” said Capt. Jennifer Andrew, the Commanding Officer of Marine Safety Unit Port Arthur. “The Coast Guard maintains one of the world’s most comprehensive and thorough vessel inspection programs, and we will continue to leverage this robust capability to ensure strict compliance with domestic and international maritime laws.”

- Between February 2022 and August 2022, a hose was connected between the incinerator waste oil tank and the sewage holding tank on the M/T Swift Winchester. This allowed oily waste to transfer into the sewage holding tank and then to be discharged directly into the sea, bypassing required pollution prevention equipment. A low- ranking engine crewmember reported this to a Superintendent at V.Ships. The Superintendent investigated the matter and discovered what appeared to be oil in the sewage tank. V.Ships dismissed the Chief Engineer. In August 2022, the new Chief Engineer ordered the engine crew to clean the Oil Water Separator (OWS) filter. The engine crew took the filter onto the deck and hosed it down with a degreaser and the oily waste washed directly overboard through a scupper.

- Coast Guard members from U.S. Coast Guard Marine Safety Unit Port Arthur conducted an examination, during which an engine room crewmember disclosed the discharges and provided photographic and video evidence documenting the illegal discharges. The M/T Swift Winchester entered Baton Rouge, Louisiana, on Aug. 25, 2022, and Port Arthur, Texas, on Sept. 7, 2022, with a knowingly falsified Oil Record Book.

· After World War II, the United States offered foreign governments a form of economic insurance: it protected sea lanes, enforced international trade

rules, and kept the dollar stable. That system was “a win-win for nearly everyone.”

But now, U.S. President Donald Trump is dismantling it.

Trump has conditioned access to American markets, forced allies to buy U.S. goods, and imperilled investments by reducing the dollar’s liquidity. In response, foreign governments are changing their economic strategies, but “not in the ways that Trump hopes,” Posen argues. U.S. allies will endure more harm than China, “the

country whose behaviour most U.S. officials want to change.” Rather than “a potentially desirable realignment” emerging from Trump’s policies, “everyone will suffer—not least the United States.”

- Fed Governor Lisa Cook Sues Trump Over Dismissal

Cook, who has not been charged with a crime, sought to retain her

position, arguing her firing was “unprecedented and illegal.

- Rapprochement. Trump’s trade war with China is pushing Bejing closer to India. China’s quiet outreach has gained momentum since March, when Xi Jinping wrote a letter to his Indian counterpart expressing concern about US deals that could hurt his country’s interests. Prime Minister Narendra Modi has welcomed the thaw as he prepares for his first visit to China in seven

years this weekend. Here’s why India increasingly needs China, and vice versa.

- Large ships may serve as collateral for Loans

India is poised to allow large ships as loan collateral, aiming to ease financing for its maritime industry. This move, coupled with the proposed Maritime Development Fund of Rs.25,000 crore and the Shipbuilding Financial Assistance Policy 2.0, seeks to boost Indian flagged ship’s global cargo share to 20% by 2047 and attract significant investment in the sector. “Lenders can accept large vessels as collateral….a decision on the minimum size of ships that can be offered will be taken in the next two months.” The average cargo handling capacity of Indian Ships engaged in Coastal trade stood at around 1,700 gross tonnage.

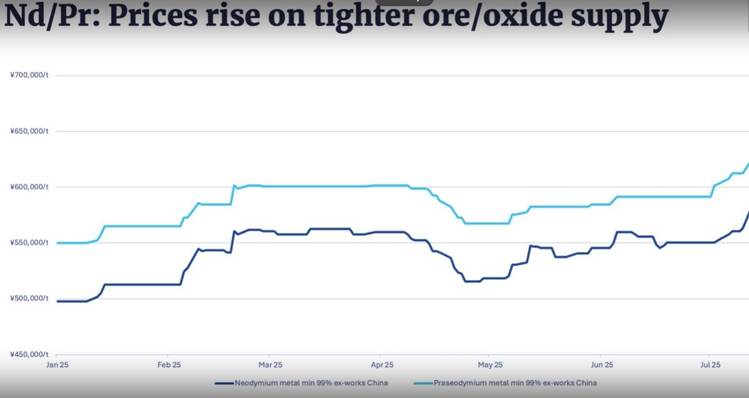

- Global Rare Earth Market Update

- Neodymium Metal min 99% and Praseodymium Metal min 99% Pricing – rise on tighter Ore/Oxide Supply

· Dry bulk FFAs pull back after hitting highest levels of 2025

- FFA pullback leads some Panamax players in South Atlantic to take notice

- Bulker freight futures took a step back on Wednesday after a surge that lifted one measure of their strength to its highest point of the year amid a surprisingly strong August.

- The Breakwave Dry Bulk Shipping ETF, a New York-listed exchange-traded fund that acts as a proxy for the bulker futures market, has fallen 3.3% so far on Wednesday, bringing it to $8.32.

- That came after the ETF ended Tuesday’s session at

$8.60 on the NYSE Arca, which was its highest closing of 2025.

- On Wednesday, Capesize forward freight agreements (FFAs) for September posted the biggest slump of the day, losing $1,529 to reach nearly $27,300 per day, according to Baltic Exchange data.

- But that is still higher than the $25,900-per-day price for September contracts a week ago, meaning the market is still retaining some of the recent gains.

- Wednesday’s futures pullback was more severe than the day’s spot market decline, which saw the Baltic Exchange’s average of Capesize earnings dip $354 to just below $24,800 per day.

· October peak

- The Capesize futures curve points to a peak of $28,200 per day in October followed by a plunge to $16,400 in January, a seasonally slow period.

- Breakwave Advisors managing partner John Kartsonas told that softness in the Pacific set a tone that led to Wednesday’s decline in Capesize futures.

- “Still, September contracts are priced at a premium to the Capesize Index, just not as much as earlier in the week when it hit $30,000”.

- “The market is quite confident that spot rates will hold firm for the next few months evident by the premiums on the futures curve.”

- Panamax futures also slumped, with September contracts dropping $641 to about $17,000 per day. That was still higher than front-month contracts’ price of $16,500 per day a week earlier.

- The day’s slump was attributed to the Capesize futures pullback.

· Spot market improvement

- The panamax FFAs dropped on Tuesday even though average spot rates moved higher. The Baltic Exchange’s Panamax Timecharter Average, which assesses spot earnings for the segment, gained $502 to approach

$16,900 per day.

- In the physical market, the futures pullback in the South Atlantic.

- “Some muted talk of the market appearing perhaps toppy

for index arrival dates, market players stepping back to

assess their physical position as the FFA market here

eased,” Baltic Exchange analysts said.

- The overall dry bulk market has had a “surprisingly solid”

August, which is typically a slow month.

- “The fact that a number of export regions, from Brazil to Australia to West Africa and North Atlantic saw strong demand simultaneously has been the main reason for the recent strength”.

- “As we look into the rest of the year, both Capes and Panamax spot rates are elevated versus recent history and if the seasonal pattern of stronger fourth quarter demand plays out this year, then we might be facing another surprisingly strong period something that is not in the mind of traders right now as the futures curve is essentially flattish.”

· Hello from Yifan in Silicon Valley :

- It’s been a busy week for the chip industry. In addition to anxiously waiting for the long-threatened semiconductor tariffs, now floated at around 300% by U.S. President Donald Trump, the biggest AI and semiconductor industry barometer Nvidia reported earnings on Wednesday.

- Despite logging another over 50% year-on-year revenue jump,

investors seemed dissatisfied. Nvidia shares dipped over

3% during extended trading Wednesday following the earnings release.

- Part of the market reaction might be because Nvidia’s road to

recovering the China market is proving to be tougher than first expected.

- While investors cheered the deal Nvidia and other chipmakers

made with the Trump administration — 15% of their revenue in exchange for China export licenses — the Chinese government is putting some new roadblocks on Nvidia’s return by calling the H20 chip, a downgraded artificial intelligence chip specially designed for the Chinese market, a “security risk.”

- However, on Wednesday, Nvidia chief Jensen Huang said he still sees China being a $50 billion market for the company this year as long as it can provide competitive products there, adding that bringing its advanced Blackwell graphics processing unit to the country is a “real possibility.”

- It reminded me of a conversation I had with a venture capitalist

from Beijing earlier this month about why the Chinese government is calling out H20 and Nvidia. In addition to the usual motive of promoting Chinese domestic chip supply, the VC suggested bashing H20 could also be the Chinese government’s way of pressuring Nvidia and Washington to open up Blackwell for export.

- I chuckled and dismissed his “conspiracy theory” way of thinking,

but now looking back, he might have been right.

- Meanwhile, another U.S. chip giant is also making headlines. Intel sold about 10% of its shares to the U.S. government in exchange for grant money from the CHIPS Act and another defence program it was already promised by previous President Joe Biden’s administration before Trump returned to the White House.

- The equity was not part of the deal under the original CHIPS Act

terms, and I distinctly remember during a briefing with Biden’s Department of Commerce officials that they told me the companies would definitely get the money as promised because it was in an enforceable “contract.” But tech companies are learning that Trump makes his own arrangements with little regard to precedent.

- Meanwhile, Trump has said that he wants to make more deals like

the one with Intel, meaning big fish like Taiwan Semiconductor Manufacturing Co. and Samsung Electronics or other smaller CHIPS Act awardees could be next.

· $2bn to $5bn worth of geopolitics

For the three-month period ended July 27, Nvidia recorded $46.7 billion in revenue, up 56% on the year and 6% higher from the previous quarter, the company announced on Wednesday.

For the third quarter, the company set expected revenue at $54 billion, plus or minus 2%. But the company’s outlook is clouded by uncertainties in China as it did not include any sales of its H20 — a downgraded artificial intelligence chip specially designed for the Chinese market — there in the estimate, Yifan

Yu reports.

In addition to its 15% revenue sharing deal with the administration of U.S. President Donald Trump yet to be “codified,” Nvidia is also facing headwinds in China as Beijing recently summoned domestic tech giants including ByteDance, Alibaba, Tencent and Baidu to discuss their use of Nvidia chips over alleged security concerns.

“We’re still waiting on several of the geopolitical issues going back and forth between the governments and the companies trying to determine their purchases and what they want to do,” Nvidia Chief Financial Officer Colette Kress said on Wednesday’s earnings call.

But if the geopolitical issues are resolved, the company estimates reaping $2 billion to $5 billion in H20 revenue for the ongoing quarter, if not more.

· SoftBank’s Son favoured by Trump

SoftBank’s Masayoshi Son has emerged as one of Donald Trump’s most favoured overseas investors, funding deals with OpenAI and Intel that have been welcomed in Washington.

- Over golf, multiple meetings in the White House and mammoth investment pledges, Son has been building close ties to Trump ever since he was first elected. Son will need to maintain that

relationship should he want control over more physical and politically sensitive assets.

- The SoftBank boss has been eyeing up Intel’s foundry business –

– both the Japanese group and the U.S. government are now shareholders — and has ambitious plans for an AI and robotics site in Arizona.

- As his commercial efforts intensify it is also the political side of his role in Washington that is causing concern for Japanese diplomats, cautiously trying to work the situation to their advantage but railing against Son’s position as a gatekeeper.

- “The dilemma is that if [Son is] not close to Trump, he’s not usable,” said Kunihiko Miyake, visiting professor at Ritsumeikan University in Kyoto and a former Japanese diplomat. “If he’s too close, it’s dangerous.”

· No China tools for 2-nanometer chips

Taiwan Semiconductor Manufacturing Co. will not use Chinese tools in its latest 2-nanometer chipmaking production lines — the most advanced in the entire industry — which will go into mass production this year, Nikkei Asia reports.

The move is to avoid any potential U.S. restrictions that could disrupt 2nm production, which is scheduled to start first in Hsinchu, Taiwan, followed by the southern Taiwan city of Kaohsiung. The Taiwanese chip titan is also building a third plant in Arizona to eventually make such chips.

TSMC’s decision was influenced by a potential U.S. regulation that could prohibit chipmakers that receive American funding or financial support from using Chinese manufacturing equipment, sources said.

- Nippon Steel to build $4bn Electric Arc Furnace mill in the US, one of it’s planned American investments for the first time. A new electric arc furnace steel mill is part of billions of dollars in

spending promised by the Japanese Company when it acquired

U.S. Steel.

- Japan to finance India Bamboo Biofuel project investing $408mn in public-private funding for a national project, to go to refinery in North Eastern region, part of the country’s effort to shift to cleaner energy.

This refinery in Assam, will soon process biofuels from bamboo.

- Rapidly warming Japan-South Korea ties leave China uneasy

- This week’s China Up Close looks at how the warming ties between Japan and South Korea can affect Chinese diplomacy. China invited South Korean President Lee Jae Myung to a military parade in Beijing to be held on Sept. 3 to commemorate the 80th anniversary of its victory against Japanese aggression. But Lee has not said “yes” yet. Instead, he flew to Japan over the weekend to meet Japanese Prime Minister Shigeru Ishiba.

- If Tokyo and Seoul are divided over historical issues, the latter could be driven closer to China. Therefore, a warmer relationship between Japan and South Korea can play a role in East Asian geopolitics. The Asia-Pacific Economic Cooperation summit and a trilateral summit among Japan, China and South Korea, both planned for later this year, are focal points to predict the future of relations among the three Asian countries as well as their regard for the U.S.

- Shippers flock to China-backed high-tech port in Peru

- Despite US concerns, official at operator CSPCP says naval use of

Chancay ‘impossible’. Ship traffic is picking up between China and Peru with the opening of a port near Lima that is majority Chinese owned and features the latest Chinese technology, slashing transportation times while alarming the U.S.

- China tests U.S. clout in South America as trade balloons 40 fold.

- China’s Xi courts Latin American leaders amid US trade tensions.

- Amid tariff crossfire, China set to widen trade with Colombia.

- Brazil courts China for coffee exports in face of still US tariffs.

- China-built ships avoid US routes as upcoming port fees roil trade.

- Trump says China must supply magnets or face possible 200% tariff.

- Japan-India-Africa Business Forum

Co-operation between Japan and India is emerging as an important dynamic in promoting development in African nations. Prominent figures from the realms of business, government and academia gathered in person and on-line in Tokyo to examine that dynamic at the Business Forum and will continue to debate this in Yokohama in August 2025.

- Global Centre for Maritime Decarbonisation study seeks to crack down on fraud in marine biofuel blends

Tracers can be used in marine supply chains without disrupting operations or affecting fuel quality. Singapore’s Global Centre for Maritime Decarbonisation (GCMD) has completed a study on

tracers to check the provenance of marine biofuel blends.

With no physical verification, biofuel supply chains are “vulnerable to adulteration, and their emissions reduction double-counted to support false subsidy claims”, the centre said.

“Recent high-profile fraud cases have underscored the need for standardised, field-verifiable methods to augment the certified sustainability claims of these biofuels.”

· Idan Ofer splashing over $1bn on latest newbuilding push

Eastern Pacific Shipping is ordering up to 14 midsize container vessels at Chinese shipyards. Eastern Pacific Shipping is stacking its massive $12bn orderbook with a move for up to 14 new container ships worth around $1.1bn.

The Idan Ofer-led company is said to have contracted two shipyards in China to build a series of 6,000-teu newbuildings to be delivered between 2027 and 2029.

· Wider sanctions working as Frontline sees higher tanker utilisation this year

John Fredriksen tanker company logs lower profit as revenue falls. John Fredriksen’s tanker company Frontline believes increased Western sanctions on shadow fleet tankers is finally having a positive effect on the mainstream fleet.

The US and Oslo-listed owner, one of the biggest global operators of VLCCs and Suezmaxes, has been a vocal critic of the international response to often elderly and poorly maintained ships trading in Russian oil.

· QSL and Compass Minerals trade blows after unpaid fees claim turns into cargo contamination spat

US minerals player says salt cargo’s contamination with iron pellets took

place at Quebec terminal.

Canadian terminal operator QSL and US-based salt producer Compass Minerals are locked in a court battle in Montreal over a salt shipment, with one company alleging unpaid fees and the other pursuing a claim for cargo contamination.

The case has been brewing in Canada’s Federal Court since January 2024 as the two sides wrangle over QSL’s efforts to secure a summary judgment on its claims.

The company, a major Canadian terminal operator, launched the litigation in Canada’s Federal Court with a claim for CAD 926,000 ($673,000) plus interest and legal costs, according to court records. It alleged that Compass Minerals Canada failed to pay invoices for stevedoring services on three bulkers. (Source: Tradewinds).

· Himalaya Shipping converts charters for two newcastlemaxes at the strongest time of the year

Changes are in line with what is currently indicated by derivatives market.

Himalaya Shipping has converted floating-rate charters for two of its vessels to fixed-rate employment during the seasonally strongest quarter of the year.

The Oslo-listed Newcastlemax Owner said the charters are fixed at a gross daily rate of $38,700 on average, plus scrubber benefits, running from 1 October to 31 December.

The conversion for the unidentified vessels is understood to be part of a hedging move by the Charterer, the name of which has not been disclosed.

· Wan Hai fire-hit boxship towed toward Middle East after 11 weeks adrift without refuge

- Europe moves to snap back Iran sanctions

- Britain, France and Germany have triggered a 30-day process to reimpose United Nations sanctions on Iran, a move that threatens to shake up tanker markets.

- The so-called snapback mechanism, launched on Thursday, would reinstate wide-ranging sanctions suspended under the 2015 nuclear accord, including restrictions on oil exports, financial flows, and maritime trade.

- Iran’s crude exports—already moving largely in the shadows via a sprawling ghost fleet of elderly tankers—would once again be designated as fully illicit under international law. Insurers, financiers and port authorities would face renewed pressure to sever ties with Iranian-linked tonnage.

- Western officials said the measure comes in response to Tehran’s

acceleration of uranium enrichment activities.

- The European move follows Donald Trump’s so-called maximum pressure campaign he has waged against Iran since his return to power in the US in January with a slew of sanctions aimed at Tehran.

· Mibau Stema grows bulker fleet backed by Hartmann-CSL venture

Denmark-based Mibau Stema Group has signed up for two new self- unloading bulk carriers at Chengxi Shipyard in China.

These newbuilds will be constructed to be biofuel- and methanol-ready as part of Mibau Stema’s strategic goal to enhance transport capabilities, increase operational versatility, and transition towards more sustainable shipping practices.

The order was made in collaboration with the Hartmann family from Germany and Canada Steamship Line (CSL). Mibau Stema said it anticipates that these new additions will not only improve transport capacity but also enhance operational flexibility within its trading network. The company currently manages a fleet of seven modern self- discharging vessels, servicing over 40 terminals along the North Sea and Baltic regions.

Mibau Stema is a partnership between Heidelberg Materials, previously known as Heidelberg Cement, and the Hartmann family. CSL and Hartmann have a well-established connection with Chengxi Shipyard.

Candeu, a joint venture between CSL and Hartmann Schiffsbeteiligungen, has previously built and owns two 40,700 dwt self- unloading vessels at the same shipyard under long-term time charter agreements with Mibau Stema.

The two new ships are scheduled to be integrated into Mibau Stema’s

fleet from September 2028.

- Mr Trump, who has slapped 50% tariffs on goods from Brazil for

the “witch-hunt” against Mr Bolsonaro.

Brazil’s wish to move on makes a striking contrast with America, which has swept the violence of January 6th 2021 under the carpet. In fact, the two countries seem to be swapping places.

Under Mr Trump, America is becoming more corrupt, protectionist and authoritarian. By contrast, Brazil is determined to safeguard and strengthen its democracy.

That brings us to this week’s and do analyses the test facing

India in its bid to become a superpower. Mr Trump has undone 25 years of American diplomacy by embracing India’s regional rival, Pakistan. And, after condemning India for buying Russian oil, he has singled out the country for 50% tariffs—like Brazil, and far

higher than a rival such as China. How should Narendra Modi,

India’s prime minister, react?

- Mr Modi must not shy away from structural changes that would boost growth and bring India closer to his aim of becoming a

$10trn economy by 2047, the centenary of its independence. For America to alienate India is a colossal mistake. For India it is a moment of opportunity: a defining test of what sort of great power it will become. (Economist).

Baltic Shipping News 28th August 2025

BALTIC INDICES 28/08/2025

DRY INDEX: 2017 (- 29)

CAPESIZE INDEX: 2884 (- 105)

PANAMAX INDEX: 1874 ( 0)

SUPRAMAX INDEX: 1461 (+14)

HANDYSIZE INDEX: 753 (+ 8)

BCI TC AVG $/DAY 23918 (- 868) BPI82 TC AVG $/DAY 16865 (0)

BSI TC AVG $/DAY 18466 (+175)

BHSI TC AVG $/DAY 13555 (+ 141) TIMECHARTER

‘Piavia’ 2011 93296 dwt dely Taichung 30 Aug trip via Indonesia redel Japan $16,000 – NS United

‘Fyla’ 2013 84104 dwt dely Campha 30 Aug trip via EC South America redel Singapore-Japan $15,000

‘Success Trader’ 2024 82231 dwt dely CJK 29 Aug trip via EC Australia redel India $15,250 opt China $16,000

‘Richland Beijing’ 2022 82022 dwt dely retro Hazira 17 Aug trip via EC South America redel Singapore-

Japan $19,250 – Raffles

‘Zhun Xing 9’ 2012 81586 dwt dely Xinsha 30 Aug trip via Indonesia redel South China $13,850 – Transtech Ocean

‘Golden Daisy’ 2015 81507 dwt dely Nagoya 2 Sep trip via Australia redel China $15,750

‘Mandarin Penghu’ 2015 81296 dwt dely Ghent 1/2 Sep trip via US east coast redel Skaw-Gibraltar

$20,500 – Tata

‘Popi S’ 2012 80337 dwt dely Barcelona 30 Aug trip via NC South America redel Skaw-Gibraltar $17,000 –

Louis Dreyfus

‘Agri Kinsale’ 2009 77171 dwt dely Yangjiang 31 Aug trip via Indonesia redel South China $13,750

‘Hoanh Son Galaxy’ 2002 76634 dwt dely Leizhou spot trip via Indonesia redel South China $14,000 –

Cambrian Bulk

‘Tian Yi 88’ 2002 76623 dwt dely Putian 5 Sep trip via Indonesia redel South China $13,500 – Cambrian Bulk

‘Aquitania’ 2006 55932 dwt dely SW Pass prompt trip redel Chittagong $23,000 – Aries

‘Nord Topaz’ 2024 39988 dwt dely Nanjing prompt trip redel Continent $15,250

‘Jian Guo Hai’ 2016 38767 dwt dely SW Pass 1/10 Sep trip redel Australia-New Zealand $17,500 – Drydel

‘Maritime Victory’ 2010 28344 dwt dely Huludao 26 Aug trip via North China redel Oman $13,000 – Lynux

‘Charbel 1’ 2011 28218 dwt dely Corpus Christi 3/4 Sep trip via Mississippi River redel Aveiro $14,000 – Quadra

PERIOD

‘W-Mayfair’ 2010 93260 dwt dely North China 1/6 Sep 10/15 months redel worldwide index linked at 93% to BPI – Swissmarine

VOYAGES ORE

‘TBN’ 170000/10 Dampier/Qingdao 13/15 Sep $10.00 fio 90000shinc/30000shinc – Rio Tinto

‘Peace’ 2010 170000/10 Tubarao/Qingdao 30 Sep/5 Oct $24.70 fio 3 days shinc/30000shinc – Mercuria

‘TBN’ 160000/10 Port Hedland/Qingdao 13/15 Sep

$10.00 fio 80000shinc/30000shinc – BHP

‘TBN’ 160000/10 Port Hedland/Qingdao 12/14 Sep

$10.00 fio 80000shinc/30000shinc – FMG

COAL

‘TBN’ 78000-82500 DBCT/Kandla-New Mangalore 20/29 Sep $19.25 fio 30000shinc/15000shinc –

Trafigura

‘TBN’ 75000/10 HPCT-DBCT-APCT/Visakhapatnam 19/28 Sep $17.70 fio 40000sshex/20000sshex – SAIL

Baltic Exchange Index – 29 AUGUST 2025 Baltic Exchange Capesize 182 Index

Route Description Value Change

===== ==========================================

C8_182 182000mt Gib/Hamburg transatlantic RV 25,869 + 37 C9_182 182000mt Cont-Med trip China-Japan 47,588 + 257 C10_182 182000mt China-Japan transpacific RV 29,026 + 664 C14_182 182000mt China-Brazil round voyage 28,691 + 365 C16_182 182000mt Backhaul 7,844 + 313

=================================================

C5TC 182 Weighted Timecharter Average 27,141 + 400

Baltic Exchange Index – 29 AUGUST 2025

Baltic Exchange Capesize Index 2925 (+ 41)

Route Description Value($) Change

====== =================================== =====

C2 160000mt Tubarao to Rotterdam 11.864 + 0.164 C3 160-170000mt Tubarao to Qingdao 24.480 + 0.045 C5 160-170000mt W Australia to Qingdao 10.200 + 0.175 C7 150-160000mt Bolivar to Rotterdam 12.907 + 0.086 C8_14 180000mt Gibraltar-Hamburg T/A RV 21,829 + 79

C9_14 180000mt Conti/Med Trip China/Japan 42,975 + 194 C10_14 180000mt China/Japan T/P RV 26,105 + 782 C14 180000mt China-Brazil RV 25,280 + 260

C16 180000mt N.China to Skaw-Passero 4,656 + 281 C17 170000mt Saldanha Bay to Qingdao 18.222 + 0.283

========================================== =======

5TC Weighted Timecharter Average 24,257 + 339

Baltic Exchange Panamax 82500mt Index 28 AUGUST 2025 Baltic Exchange Panamax Index 1,874 ( 0)

Route Description Value ($) Change

====== ================================= ======== P1A_82 Skaw-Gib T/A RV 19,300 + 240

P2A_82 Skaw-Gib trip HK-SKorea incl Taiwan 26,463 + 66 P3A_82 HK-SKorea incl Taiwan, Pacific/RV 14,394 – 212 P4_82 HK-SKorea incl Taiwan to Skaw-Gib 8,662 – 45 P6_82 Dely Spore Atlantic RV 16,430 – 31

====== ================================= =======

P5TC Weighted Timecharter Average 16,865 – 0

The following routes do not contribute to the BPI or Weighted TC Average.

Route Description Value ($) Change

====== ================================= ======== P5_82 S. China Indo RV 14,494 + 77

P7 66000mt Mississippi Rvr to Qingdao 56,314 + 0.021 P8 66000mt Santos to Qingdao 40,436 – 0.085

Baltic Exchange Panamax 82 Asia Index – 29 AUG 2025

Route Description Size (MT) Value($) Change

===== ====================== ======== ======

P5_82 S.China one Indo RV 14,256 -238

Baltic Exchange Supramax Index – 28 AUGUST 2025 Baltic Exchange Supramax Index 1461 (+ 14)

Route Description Value ($) Change

| ====== | ========================================= | ||

| S1B_63 | Cnkle trip via Med or B.Sea to China-.Kor 18,817 + 267 | ||

| S1C_63 | US Gulf trip to China-South Japan 28,764 + 321 | ||

| BS2_63 | North China one Australian or Pacific RV 16,921 + 71 | ||

| BS3_63 | North China trip to West Africa | 16,500 | 0 |

| S4A_63 | US Gulf trip to Skaw-Passero | 29,857 | + 448 |

| S4B_63 | Skaw-Passero trip to US Gulf | 13,907 | + 186 |

| BS5_63 | West Africa trip via ECSA to N. China | 19,921 | + 260 |

| BS8_63 | South China trip via Indo to EC.India 21,079 + 171 | ||

| BS9_63 | W.Africa trip via ECSA to Skaw-Passero 16,693 + 332 | ||

| S10_63 | S.China trip via Indonesia to South China 16,664 + 100 | ||

| S15_63 | Indian Ocean trip via S.Afr to Far East 14,217 + 175 | ||

| ====== | =========================================== | ||

| S11TC | Weighted Timecharter Average 18,466 + 175 | ||

S10TC Supramax(58) Timecharter Average 16,060 + 175

Baltic Exchange Supramax Asia Index – 29 August 2025

Route Description Value($) Change

====== =============================== =======

S2_63 N.China one Austr or Pac RV 17,007 + 86 S8_63 S.China via Indonesia/Ec India 21,000 – 79 S10_63 S.China via Indo/S.China 16,593 – 71

====== =============================== =======

S3TC Weighted Time Charter Average 18,045 – 7

Baltic Exchange Index – 28 AUGUST 2025 Baltic Exchange Handysize Index 753 (+ 8)

Route Description Value ($) Change

====== ========================================

HS1_38 Skaw-Pass trip Recalada – Rio de Janeiro 8,107 + 107 HS2_38 Skaw-Passero trip Boston-Galveston 10,357 + 178 HS3_38 Rio de Janeiro-Recalada trip Skaw – Pass 18,300 + 550 HS4_38 USGlf trip via USG or NCSA to Skaw-Pass 18,308 +129 HS5_38 SE Asia trip to Spore – Japan 13,850 + 25 HS6_38 N.China-S.Kor-Jpn trip to N.China-S.Kor-Jpn 13,013 +82 HS7_38 N.China-S.Kor-Jpn trip to SE Asia 12,981 – 7

====== ===========================================

7TC Weighted Timecharter Average 13,555 + 141

(c) Baltic Exchange Information Services Ltd., 2025

Marex Media

The Author

Mr Bansi Jaising – photo you have

All Rights Reserved “Disclaimer”

All Rights in material and information in this document is reserved. Any form of reproduction or distribution of the information contained in this by any means whether electronic or otherwise is expressly prohibited including distribution by re- producing it anywhere.

I do not guarantee the adequacy, accuracy, timeliness, and/or completeness of the Data or any component thereof or any communication (written, oral, electronic, or other format). The writer shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive, or consequential damages (including but not limited to, loss of profits, trading losses, and loss of goodwill).

The data provided here is sourced from various news media, bulletins and reports from various sources to which I do not have any claim.

Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management or other decision.

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables, images in this Publication, at your own risk or consequences and is only for your personal use.